-

S&P 500 is now 10% below its end-July peak; set for third straight monthly drop

- Relief for equity bulls may depend on 4 key events in first 3 days of November

-

Events watchlist: US Treasury announcement, FOMC decision, Apple earnings, US jobs report

-

Current technical pullback may be short-lived; bulls need fundamental boost

- S&P 500 may see third consecutive weekly move of over 2%

The S&P 500 has entered a technical correction, which is when an asset’s price falls by over 10% from a recent peak.

Note that the SPX500_m posted a closing price on Friday (October 27th) that was 10.3% lower than its closing price registered on July 31st (its year-to-date high).

Furthermore, the SPX500_m is set to post a third straight month of declines – something not seen since Q1 2020 at the onset of the pandemic.

Here’s how this blue-chip stock index has fared recently:

-

August: down 1.77%

-

September: down 4.87%

- October so far (as of market's close on Friday, October 27th): down 4%

Amidst such a gloomy backdrop, hopes for an SPX500_m rebound this week are set to rest on these 4 major events:

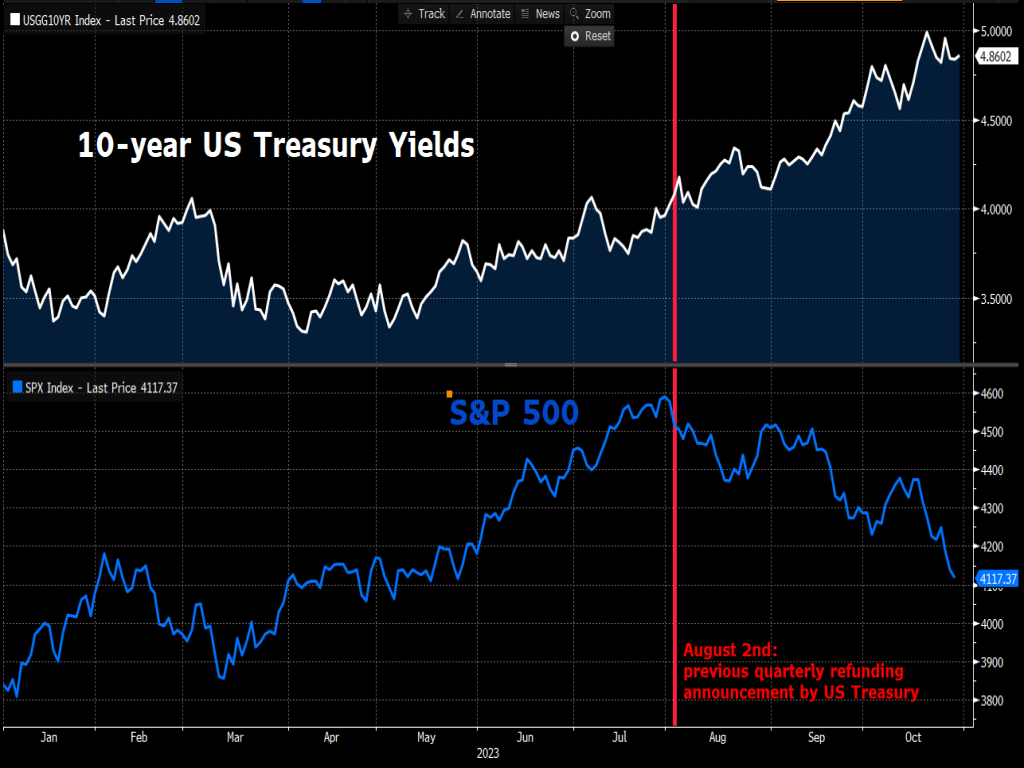

1) Wednesday, November 1st: US Treasury quarterly refunding announcement

This is when the US government reveals how much new debt it has to sell to markets to keeping funding its budget.

To underscores the sheer importance of this upcoming announcement for global markets, note how the prior quarterly refunding announcement on August 2nd sparked a rout in US bond markets, setting 10-year US Treasury yields on the way to hitting 5% for the first time since 2007!

NOTE: Yields rise with bond prices fall.

At the same time, the S&P 500 has been on a steady decline since that last announcement in early August.

This is because, higher yields on US Treasuries (deemed to be the “safest” investment in the world) makes riskier assets, such as stocks, less appealing.

For this week’s announcement, markets expect US$114 billion worth of securities to be outlined for sale by the US Treasury.

POTENTIAL SCENARIOS:

-

A higher-than-expected figure (US Treasury intends to sell more bonds than markets expect) could translate into another leg up for US Treasury yields, and perhaps extend the drop seen in the SPX500_m.

- A lower-than-$114 billion number revealed by the US Treasury, or efforts to subdue its refunding costs, may offer some relief for SPX500_m.

2) Wednesday, November 1st: FOMC rate decision

To be clear, the Fed is roundly expected to leave its benchmark rates unchanged this week.

Furthermore, Fed Chair Jerome Powell is also set to reiterate his “higher for longer” message, which is something that markets are fully aware of.

POTENTIAL SCENARIOS:

-

If Chair Powell can strike a more hawkish tone, perhaps going into more detail as to just how much “longer” the Fed will keep its benchmark rates elevated, that could spark more declines for the SPX500_m.

- However, if Chair Powell were to close the door on any further rate hikes, or perhaps even concede that the first Fed rate cut may actually arrive sooner than expected (markets currently predict it’ll happen in June 2024), that could help the SPX500_m recover.

3) Thursday, November 2nd (after US markets close): Apple earnings

Apple has a market cap of US$2.63 trillion, making it the world’s most valuable company.

Apple alone accounts for about 7% of the total S&P 500, making it the largest stock on this benchmark index that is tracked by our SPX500_m.

Given Apple’s sheer size, how markets react to its earnings would have a large influence over how the S&P 500 performs.

Keep in mind that Apple is facing its longest sales slump in over 20 years, and is now facing slowing sales of its iPhone 15 in China.

NOTE: China accounts for about 20% of Apple’s total revenues.

Hence, both its backward-looking Q4FY23 numbers, as well as forward-looking statements especially around Chinese sales, could dictate how Apple’s share prices react.

Also, Apple’s share price is expected to move by 3.77%, either upwards or downwards, on Friday, November 3rd - the day after the company unveils its financial results for the July-September period (the fourth quarter of the company’s 2023 fiscal year).

POTENTIAL SCENARIOS:

-

Better-than-expected earnings out of Apple, or if the company sounds optimistic about a turnaround in China, could help pull the SPX500_m out of a technical correction.

- Disappointing Apple earnings and/or more concerns about a prolonged sales slump, could push the SPX500_m deeper into a technical correction.

4) Friday, November 3rd: US jobs report

As is the case on the first Friday of most months, markets are eagerly anticipating the tier-one US nonfarm payrolls report.

Here are the current forecasts for some of October's key figures:

-

Headline NFP number: 190,000 new jobs added to the US labour market in October

(this would be its lowest tally since June 2023's 105,000 figure)

-

Unemployment rate: 3.8%

(this would match September's unemployment rate)

-

Average hourly earnings: 4% year-on-year (October 2023 vs. October 2022)

(this would be slightly lower than September's 4.2% year-on-year number)

-

Average hourly earnings: 0.3% month-on-month (October 2023 vs. September 2023)

(this would be slightly faster than September's 0.2% month-on-month number)

POTENTIAL SCENARIOS:

-

Evidence of a stronger-than-expected US jobs report may indeed allow the Fed to maintain its benchmark rates "higher for longer", or perhaps even pave the way for one more 25-basis point hike in this cycle.

Such expectations could heap more downward pressure on the SPX500_m.

-

Cracks showing in the US labour market, suggesting that the world's largest economy is bearing the brunt of all those Fed rate hikes since last year, may seal the door shut on a further Fed rate hike, and potentially pave the way for a sooner-than-expected Fed rate cut,

Such expectations may spark joy among SPX500_m bulls (those hoping prices will go up).

From a technical perspective …

At the time of writing, the SPX500_m is seeing a technical rebound, as its 14-day relative strength index attempts to recover from the 30 line which denotes “oversold” conditions.

However, this technical rebound may prove short-lived, and bulls would need a fundamental catalyst to push the SPX500_m higher going into November.

POTENTIAL RESISTANCE:

-

4152.2: lower bound of downtrend since July

-

4200: psychologically-important level which had repelled bulls on several occasions in 1H23

(also, 38.2 Fibonacci retracement level from October 2022- July 2023 ascent)

- 200-day simple moving average (SMA)

POTENTIAL SUPPORT:

-

4106: intraday low on Friday, October 27th

- 4052.2: mid-way (50 Fibonacci retracement level) from October 2022- July 2023 ascent