REMINDER: 11 of FXTM’s 18 stock indices have reached their respective record highs so far in 2024.

However, upon closer inspection, not all stock indices are created equal.

First, there are the outperformers:

-

US500: up 9% year-to-date

-

EU50: +10.9%

-

TWN: +11.9%

-

NETH25: +13.4%

- JAP225: +18.1%

At the other end of the spectrum, there are others that are clearly lagging behind their peers, with more conservative year-to-date gains:

-

US30: +2%

-

UK100: +3.4%

- CN50: +3.6%

Over the coming week, these 3 events could either boost, or further dampen, the above-listed “laggards”:

1) US30 index: Goldman Sachs earnings (Monday, April 15th)

Wall Street banking giant, Goldman Sachs, is the 3rd-largest member of the US30 stock index.

NOTE: The US30 tracks the benchmark Dow Jones Industrial Average index a.k.a. the Dow

Goldman Sachs alone accounts for 6.8% of the Dow!

And at the time of writing, markets predict that Goldman Sachs’s share prices could move 3.4%, either up or down, once US stock markets reopen after the bank has released its earnings.

Hence, the market’s reaction to Goldman Sachs’s earnings could have a large impact on the US30’s performance.

-

Better-than-expected earnings for Goldman Sachs could lift the US30 towards its 50-day simple moving average (SMA).

- Worse-than-expected earnings for Goldman Sachs could sink the US30 towards its 100-day SMA, where also lies the psychologically-important 38,000 line.

2) CN50 index: China’s key economic data releases (Tuesday, April 16th)

The world’s second-largest economy is due to release its 1Q GDP data, alongside last month’s performance for industrial production, retail sales, retail sales, and property investment.

Essentially, this coming Tuesday ...

Investors and traders are about to be hit with a lot of information on how the Chinese economy is faring right now.

Note that the CN50 index’s performance is very much tied to the overall health of the Chinese economy.

After all, stocks within the financial, consumer staples, and industrials sectors combine to account for two-thirds (67.8%) of the entire CN50 index.

Hence, no surprise that the CN50 has lagged, given the economic challenges that China’s currently facing.

-

If Tuesday’s data releases come in better-than-expected, this could send CN50 back above the psychologically-important 12,000 mark and past its 200-day SMA.

- However, evidence of a still-sluggish Chinese economy may keep the CN50 index subdued below its 50-day SMA, and potentially on a path towards that end-Feb/early-March low of 11,686.3.

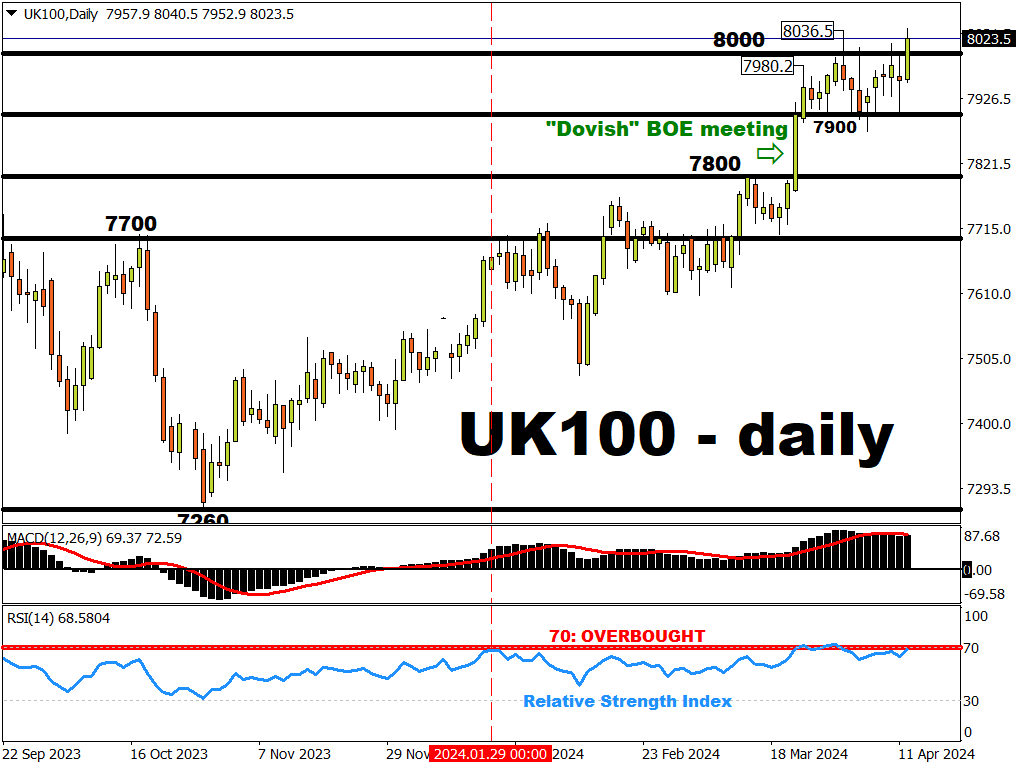

3) UK100 index: UK March consumer price index (Wednesday, April 17th)

NOTE: The consumer price index (CPI) measures inflation in an economy.

Economists predict that the March UK CPI rose by:

-

2.9% year-on-year (March 2024 vs. March 2023)

- 0.4% month-on-month (March 2024 vs. February 2024)

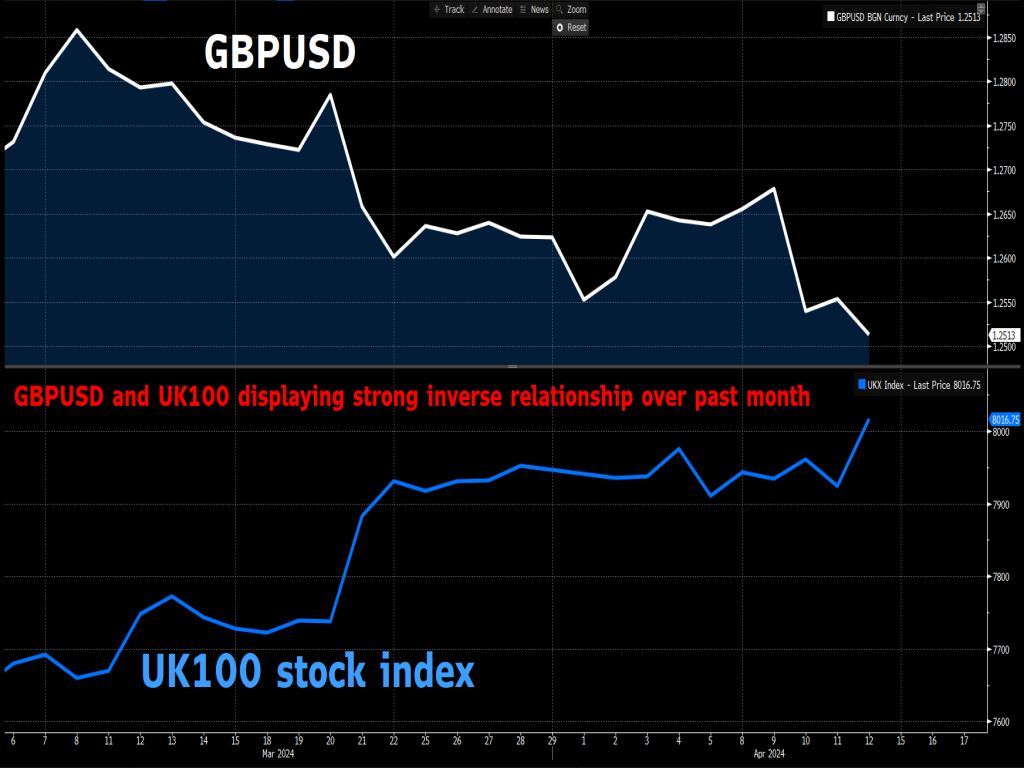

Recall that the UK100 index has an inverse relationship with the British Pound (GBP).

NOTE: When GBP goes up, the UK100 tends to fall, and vice versa.

This inverse relationship has been particularly evident over the past month:

The primary reason for the price moves in the above chart (GBPUSD vs. UK100) is because ...

Markets are now betting that the Bank of England’s (BOE) interest rate CUTS will be brought forward.

Such revised expectations have dragged GBPUSD to its year-to-date low closer to 1.2500, while the UK100 has made multiple breaches of the psychologically-important 8,000 mark.

-

Higher-than-expected CPI figures, that force the BOE to delay its rate cuts, could strengthen Sterling and drag the UK100 back below the 8k mark.

- Lower-than-expected CPI figures, that allow the BOE to bring forward its rate cuts, could weaken GBP and help keep the UK100 above 8,000.

Overall, FXTM’s stock indices should see enough triggers to move in the coming week.

For further consideration, here’s a more comprehensive list of scheduled events that could move various asset classes over the coming week:

Monday, April 15

- CNH: PBoC rate decision

- EUR: Eurozone February industrial production

- USD index: US March retail sales; speeches by Dallas Fed President Lorie Logan, San Francisco Fed President Mary Daly

- US30 index: Goldman Sachs earnings

Tuesday, April 16

- CN50 index: China 1Q GDP; March industrial production, retail sales, unemployment, property investment

- EU50 index: Eurozone April ZEW survey; February trade balance

- GBP: UK February unemployment

- RUS2000 index: US March industrial production

- CAD: Canada March CPI

- US500 index: Morgan Stanley, Bank of America earnings

Wednesday, April 17

- NZD: New Zealand 1Q CPI

- JP225 index: Japan March trade balance

- SG20 index: Singapore March exports

- NETH25 index: Eurozone March CPI (final)

- UK100 index: UK March CPI; speech by BOE Governor Andrew Bailey

- US400 index: Fed Beige Book; speeches by Cleveland Fed President Loretta Mester, Fed Governor Michelle Bowman

Thursday, April 18

- AUD: Australia March unemployment; 1Q business confidence

- TWN index: TSMC earnings

- USD: US weekly initial jobless claims; speeches by Fed Governor Michelle Bowman, New York Fed President John Williams, Atlanta Fed President Raphael Bostic

Friday, April 19

- JPY: Japan March national CPI

- GER40 index: Germany March PPI

- GBP: UK March retail sales

- USD: Speech by Chicago Fed President Austan Goolsbee