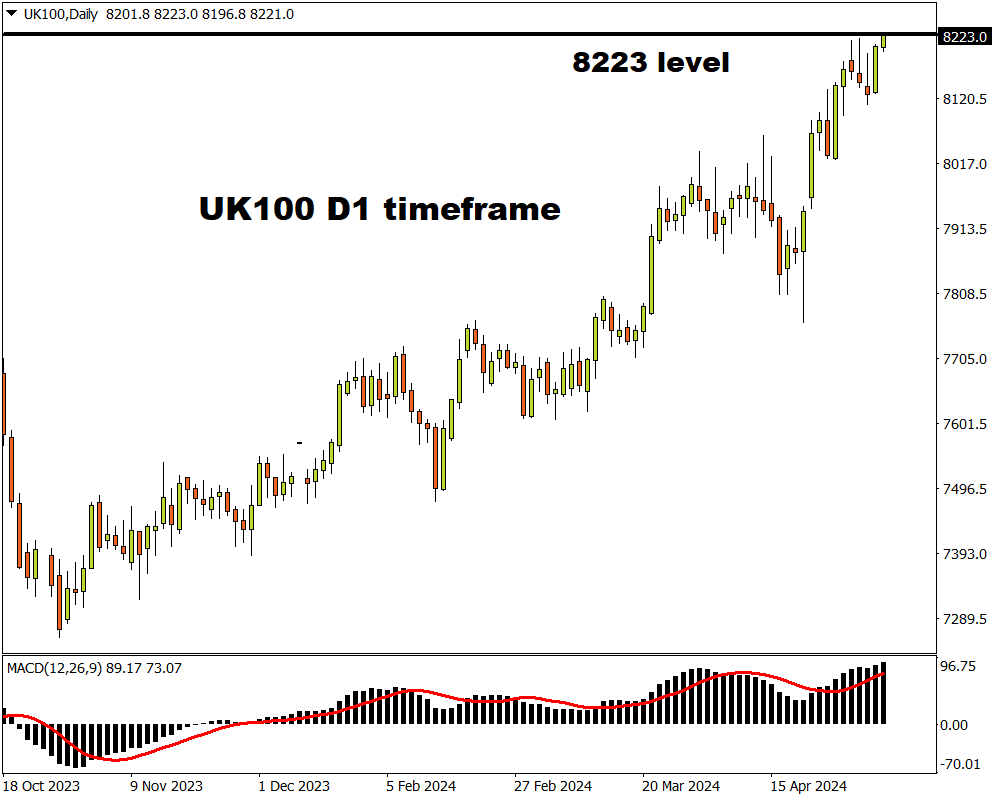

- UK100 ↑ over 2% in April

- Index could see heightened volatility

- BoE decision & Q1 GDP in focus

- Bullish on D1 but RSI overbought

- Key levels of interest at 8200, 8110 & 8023

Even as the clock ticks down to the US jobs report this afternoon (Friday, 3rd May), markets are bracing for more action in the week ahead.

Key central bank decisions, top economic data, and another volley of corporate earnings could present fresh trading opportunities:

Monday, 6th May

- CN50: China Caixin services PMI

- EU50: Eurozone S&P Global Services PMI, PPI

- CHF: SNB President Thomas Jordan speech

- US500: New York Fed President Williams, Richmond Fed President Barkin speech

Tuesday, 7th May

- CNH: China forex reserves

- AU200: RBA rate decision

- EU50: Eurozone retail sales

- GER40: Germany factory orders

- TWN: Taiwan CPI

- USD: Minneapolis Fed President Neel Kashkari

- US30: Walt Disney earnings

- UK100: BP earnings

Wednesday, 8th May

- GER40: Germany industrial production

- SEK: Riksbank rate decision

- TWN: Taiwan trade

- USD: Fed Governor Lisa Cook speech

- JP225: Toyota earnings

Thursday, 9th May

- CN50: China trade

- JP225: BoJ summary of opinions

- ZAR: South Africa manufacturing production

- USD: US initial jobless claims

- UK100: BoE rate decision

Friday, 10th May

- CAD: Canada unemployment

- JP225: Japan household spending

- EUR: ECB meeting minutes

- NZD: New Zealand home sales, PMI

- USD: University of Michigan consumer sentiment, Chicago Fed President Goolsbee speech

- UK100: UK industrial production, Q1 GDP, BOE Chief Economist Huw Pill speech

FXTM’s UK100 caught our attention this morning after kissing a fresh all-time high.

Note: UK100 tracks the FTSE100 index – the benchmark measuring the stock performance of the 100 largest listed companies on the London Stock Exchange.

After ending April over 2% higher and hitting record highs along the way, it looks like the FTSE100 has got its mojo back. Bulls have been supported by easing geopolitical risks and expectations around the BoE cutting interest rates by August.

With all the above said, the week ahead could be volatile for the UK100!

Here are 3 reasons why:

1) BoE rate decision

The Bank of England is widely expected to leave interest rates unchanged next week.

So much focus will be directed towards the policy statement, BoE Bailey’s news conference and the quarterly Monetary Policy Report (MPR) – making it a super Thursday combo.

Note: Over 80% of the revenues from FTSE100 companies come from outside of the UK.

So essentially, when the pound appreciates, it results in lower revenues for those companies that acquire sales from overseas – dragging the UK100 lower as a result. The same is true vice versa.

Traders are currently pricing in a 45% probability of a 25-basis point BoE cut by June with this jumping to 89% by August.

- The UK100 could push higher if the pound weakens on any hints around lower UK rates.

- Should a hawkish-sounding BoE boost the pound, the UK100 could fall.

2) Key UK data

Beyond the BoE rate decision, all eyes will be on first-quarter GDP figures published on Friday.

Markets expect a modest quarter-on-quarter growth of 0.4% as the economy rebounds from the mild recession in the second half of 2023. Also, keep an eye on the latest industrial production figures which could provide additional insight into the health of the UK economy.

- Should the data support the case for lower UK interest rates, this could support the UK100.

- If the reports push back BoE cut bets – this may hit the UK100 as the pound strengthens.

Note: On the earnings front, BP’s latest results published on Tuesday could trigger volatility as it accounts for just over 4% of the FTSE100 weighting.

3) Technical forces

The UK100 is firmly bullish on the daily charts with prices above the 50, 100 and 200-day SMA. However, the Relative Strength Index indicates that overbought conditions have been reached.

- A solid weekly close above 8200 may encourage a move towards the next psychological level at 8300.

- Should prices slip below 8200, this could trigger a decline towards 8111 and potentially 8023 before bulls jump back into the scene.