- Raft of UK data could rock UK100 this week

- UK CPI sparked moves of ↑ 0.9% & ↓ 0.8% over past year

- Incoming US CPI data may set tone for markets

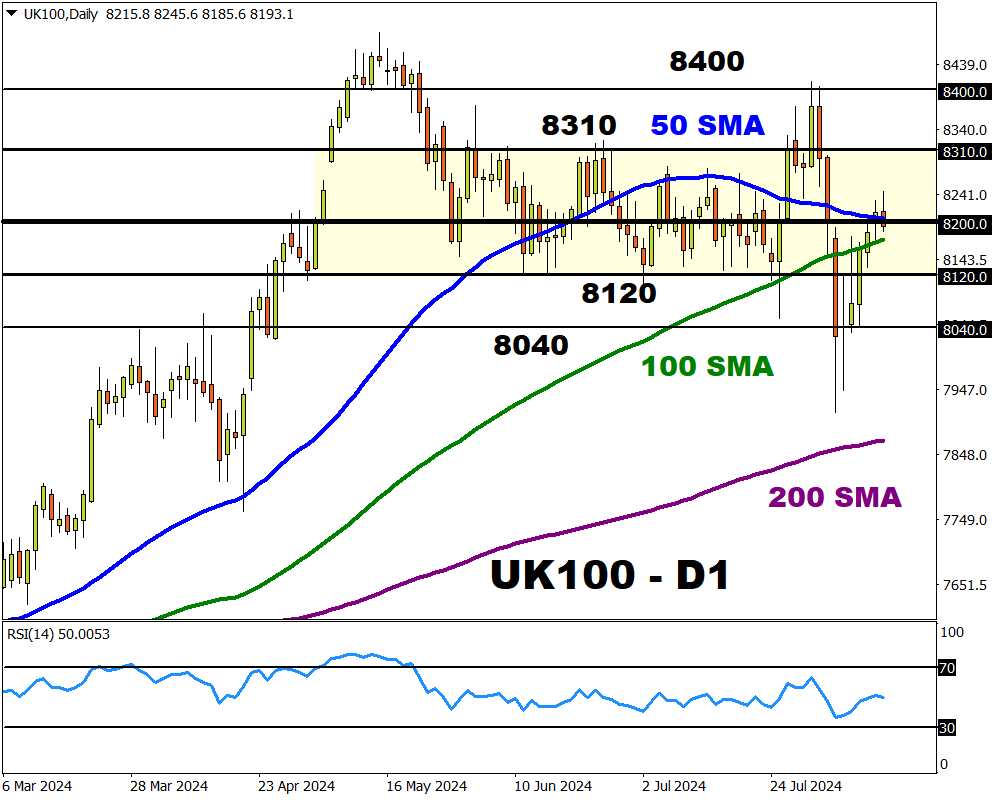

- Key levels of interest – 8120, 8200, 8310

Watch this space because FXTM’s UK100 index could see significant price swings!

That’s right, a raft of UK economic data over the next few days may inject the stock index with fresh volatility. We have already seen some action this morning after a surprise drop in the UK’s unemployment rate for June triggered a selloff.

The strong jobs data cooled bets around BoE rate cuts – boosting the British Pound as a result.

Note: Over 80% of the revenues from FTSE100 companies come from outside of the UK. When the pound appreciates, it results in lower revenues for those companies that acquire sales from overseas – dragging the UK100 lower as a result. The same is true vice versa.

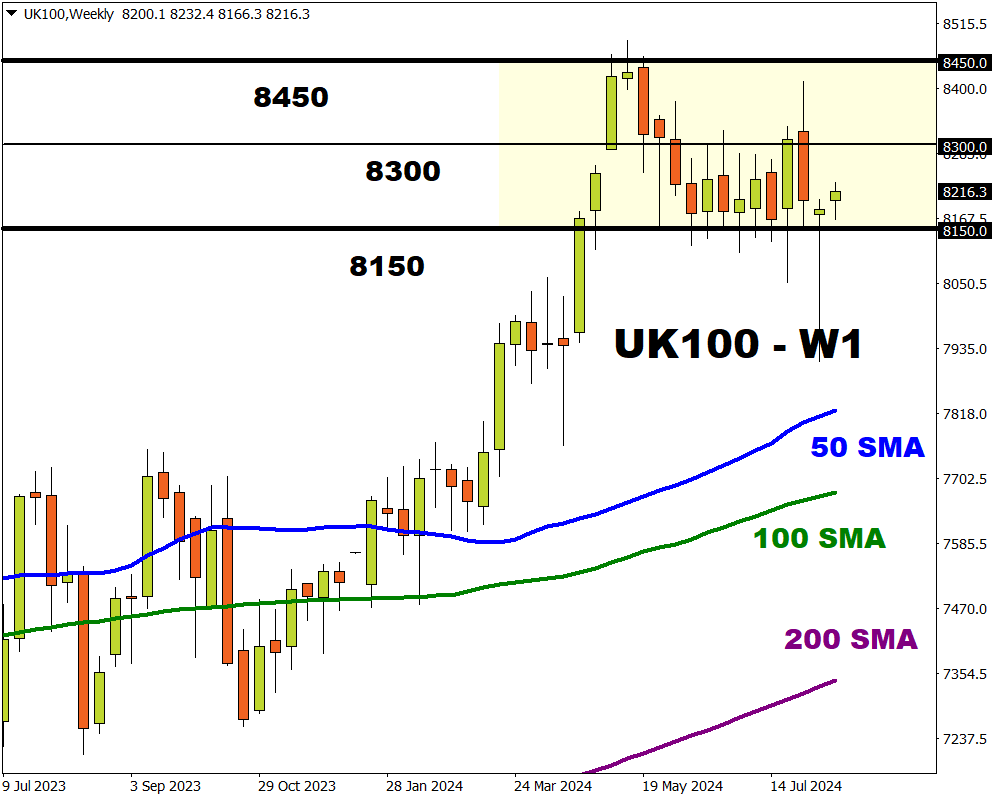

Despite the aggressive selloff last Monday, prices remain trapped within a range on the weekly charts with support at 8150 and resistance at 8450.

Note: UK100 tracks the FTSE100 index – the benchmark measuring the stock performance of the 100 largest listed companies on the London Stock Exchange.

With all the above said, here are 3 major economic events that may trigger significant volatility:

1) UK July CPI report – Wednesday, 14th August

The incoming consumer price index report may influence bets around when the BoE will cut rates again in 2024.

Markets are forecasting:

- CPI year-on-year (July 2024 vs. July 2023) to rise 2.3% from 2.0% in the prior month.

- Core CPI year-on-year to cool 3.4% from 3.5% in the prior month.

- CPI month-on-month (July 2024 vs June 2024) to cool 0.1% from 0.1% in the prior month.

UK inflation rate is expected to have risen in July. If the incoming figures confirm this, then this may push back BoE cut bets.

Golden nugget: Over the past year, the UK CPI report has triggered upside moves on the UK100 as much as 0.9% and declines of 0.8% in a 6-hour window post-release.

2) UK Q2 GDP data – Thursday 15th August

Beyond the UK CPI report, all eyes will be on second-quarter GDP figures published on Thursday.

Markets expect a modest quarter-on-quarter growth of 0.6%, slightly slower than the 0.7% seen in Q1. Also, keep an eye on the latest industrial production figures which could provide additional insight into the health of the UK economy.

- Should the data support the case for lower UK interest rates, this could boost the UK100.

- If the reports push back BoE cut bets – this may hit the UK100 as the pound strengthens.

Golden nugget: Over the past year, the UK GDP report has triggered upside moves on the UK100 as much as 0.7% and declines of 0.6% in a 6-hour window post-release.

3) US July CPI

Outside of the United Kingdom, all eyes will be on the US July inflation report published on Wednesday.

Markets remain edgy due to the weak jobs report earlier this month with US recession fears lingering in the air. The incoming US CPI report may shape expectations around aggressive Fed rate cuts this year.

Traders have already priced in a 25-basis point move next month with a 50% probability of a 50-basis point cut.

Given how this key report may set the tone for markets, indices across the globe including the UK100 may be impacted.

4) Technical forces

On the technical front, the UK100 is flirting around the 50 and 100-day SMA with prices still trapped within a range. The index could be waiting for a potent fundamental spark to trigger its next significant move either up or down.

- A strong daily close above 8200 could encourage a move higher toward 8310 and 8400.

- Should prices dip below the 100-day SMA, this could encourage a decline to 8120 and 8040.