- Domestic NZ inflation pressures ease, but remain elevated

- RBNZ likely to deliver a third jumbo rate cut on Feb 19

- Kiwi acting as a proxy for US trade policy, especially towards China

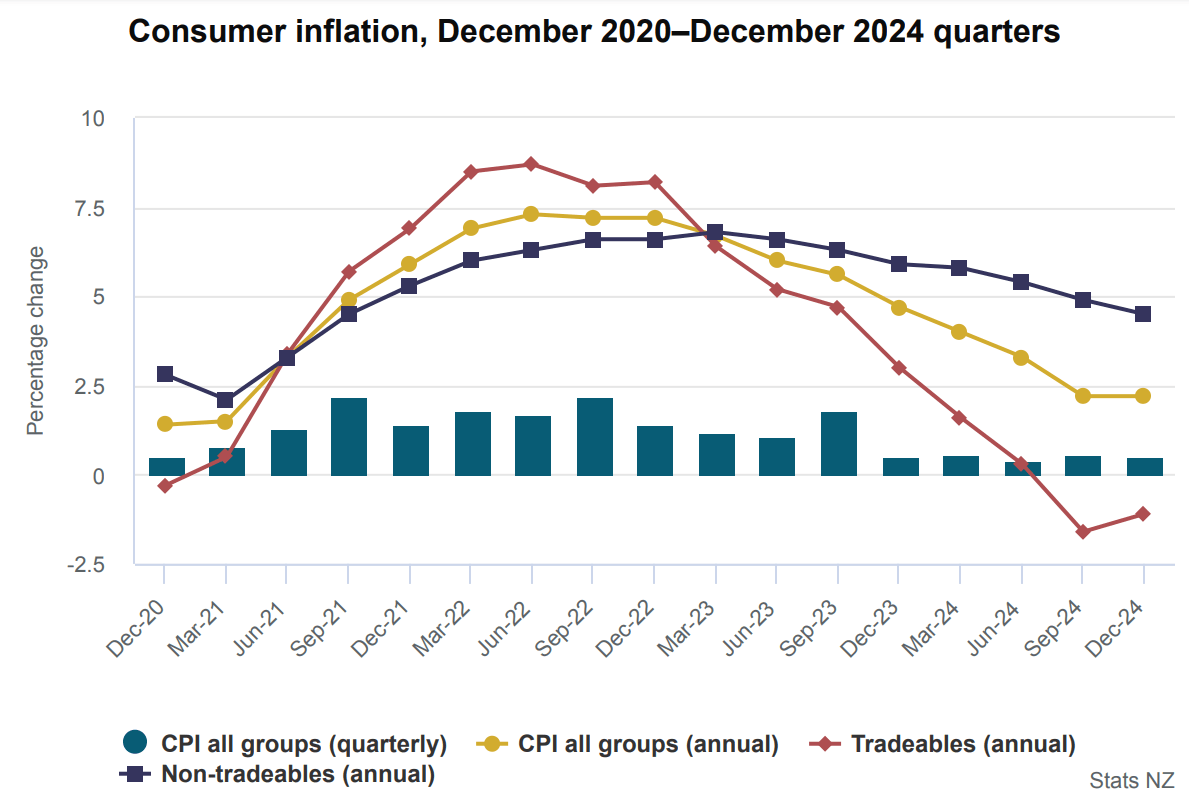

Inflation Overshoots but Remains Cool

New Zealand consumer price inflation came in slightly hotter than both market and RBNZ expectations for the December quarter. However, the overshoot doesn’t appear significant enough to derail expectations for another likely supersized rate cut from the bank in February.

Headline inflation rose 0.5% for the quarter and 2.2% over the year—just a tenth above market and RBNZ forecasts. While marginally higher than policymakers anticipated, the annual rate remained unchanged from Q3 and sits within touching distance of the RBNZ’s 2% inflation target midpoint.

Source: StatsNZ

Breaking down the data, non-tradable inflation—which reflects prices driven by domestic factors—slowed to 4.5% annually from 4.9% in September. In contrast, tradable inflation, more influenced by international conditions, rose 0.3% for the quarter but fell 1.1% over the year.

The broader theme persists: sticky domestic inflation continues to be offset by weak international price pressures. That said, with the New Zealand dollar weakening sharply in recent months, the sustainability of this offset looks increasingly uncertain.

Core inflation—excluding food, household energy, and vehicle fuels—remained stubborn, rising 0.9% for the quarter and 3% annually. This represents only a slight deceleration from Q3, leaving core inflation perched at the top of the RBNZ’s target band with sluggish progress overall.

The RBNZ’s preferred measure of underlying inflation—the sectoral factor model—will be released at 2pm Wellington time on Wednesday. This measure increased by 3.4% in the year to September 2024.

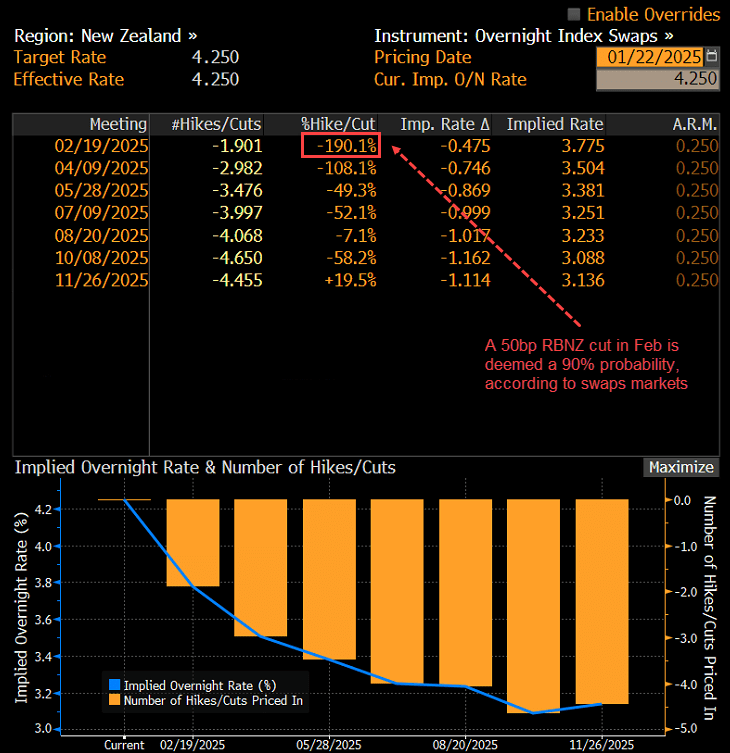

Third Jumbo RBNZ Rate Cut Priced

Market pricing for the RBNZ’s cash rate outlook is largely unchanged following the inflation report. Swaps markets now imply a 90% probability of another 50bp cut on February 19, adding to the two delivered earlier in the cycle. More than 100bps of cuts remain priced in for the remainder of 2025.

Source: Bloomberg

Domestically, the only major data release that could challenge expectations for a 50bp cut is the Q4 labour force survey, scheduled for February 5.

NZD/USD May Have Bottomed Near-Term

With New Zealand’s rates outlook largely unchanged, international factors will likely continue to dominate NZD/USD movements. The bullish break of the downtrend dating back to mid-November suggests recent lows for the Kiwi may be in. Tuesday’s dip below that level proved unsustainable, and momentum indicators have swung bullish.

Source: TradingView

Should NZD/USD manage to climb and hold above 0.5700, it could spark a quick move toward 0.5774 where the pair briefly stalled before its latest leg lower.

For now, the Kiwi’s behaviour reflects its role as a risk barometer for US trade policy. With Donald Trump failing to introduce tariffs via executive orders in his first two days in office, there’s a narrow window for NZD/USD to push higher on hopes that trade agreements will be forged through negotiation rather than punitive measures.

-- Written by David Scutt

Follow David on Twitter @scutty