Markets are enjoying the fading turmoil from the banking crisis with the Nasdaq 100 especially notable with its recent outperformance. The tech-laden index is up over 20% from its December lows as megacap growth stocks lap up the lower interest rate environment sparked initially by the recent market upheaval. The longer-term impact of the turmoil is yet to sink into the wider economy. But tighter credit and potential regulations will have a dampening effect on economic activity and may also curb the Fed’s appetite for higher rates ahead.

This means the dollar could find it hard to strengthen significantly going forward. We did get positive US consumer confidence data earlier this week which surprised to the upside. Recent market jitters and focus on the risk of a US recession saw low expectations for the data. But the strong job market seems to be supporting sentiment and eyes will soon turn to the latest non-farm payrolls report next Friday.

In the near-term, today’s calendar sees the final release of the fourth quarter US GDP figures. These are backward-looking but will inform on how the economy entered the new year. All eyes will then swiftly turn to tomorrow’s US core PCE data. This is the Fed’s favoured inflation gauge as it is a far broader measure of inflation than just the widely watched CPI numbers, which are only based on survey data from consumers. Hopes are high that price pressures show a further decline, and there will be a lot of attention on services inflation which is proving sticky.

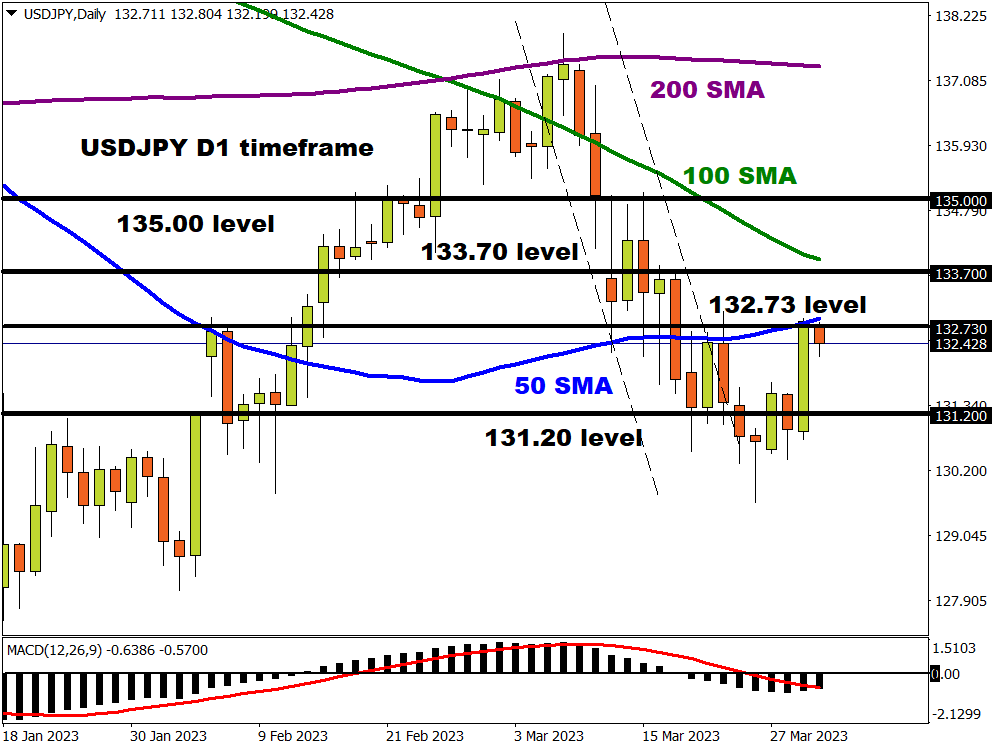

Month-end and quarter end flows affecting USD/JPY

The yen has been hit from two sides this week. Better risk sentiment has seen the safe haven JPY suffer. Higher Treasury yields as markets unwind dovish Fed bets have also supported buyers in USD/JPY, while month-end and quarter-end flows are said to act as additional headwinds. The major has hit the 50-day simple moving average at 132.73. The halfway point of the 2022 rally sits close by as further resistance at 132.70.

USD/CAD breaking down

The CAD has been in the doldrums recently as commodities struggled. Interestingly, the latest CFTC data release, which shows positions held by major hedge funds and commercial speculators, highlighted the biggest net short in the loonie since 2008. For contrarian traders, this type of signal can provide a chance to run against the prevailing “wisdom of the crowd”.

That is pretty much what we’ve seen this week as better risk sentiment and oil prices have helped the highly commodity-sensitive currency. The major printed a “doji” candlestick earlier this month after hitting a five-month high at 1.3862. That top got close to long-term trendline resistance going back to the March 2020 spike. The “doji” warned of indecision and since then prices have traded around 1.37 and a minor Fib level (23.6%) of the August rally at 1.3682, before breaking down earlier this week. The 50-day simple moving average at 1.3538 may act as initial support with the 100-day moving average at 1.3516.