Despite the holiday-shortened week ahead for US and UK financial market, the US March nonfarm payrolls (NFP) report is set to grab hold of traders and investors’ attentions.

The NFP is due at the end of a week that also features these economic data releases and events:

Monday, April 3

- CNH: China March Caixin manufacturing PMI

- EUR: Eurozone March manufacturing PMI

- GBP: UK March manufacturing PMI (final)

- USD: US March ISM manufacturing

Tuesday, April 4

- AUD: Reserve Bank of Australia rate decision

- GBP: Bank of England Chief Economist Huw Pill speech

- USD: Cleveland Fed President Loretta Mester speech

Wednesday, April 5

- AUD: RBA Governor Philip Lowe speech

- EUR: Germany February factory orders; Eurozone composite and services PMIs (final); speech by ECB chief economist Phillip Lane

Thursday, April 6

- AUD: Australia February trade balance

- CNH: China March composite and services PMIs

- EUR: Germany February industrial production

- CAD: Canada March unemployment

- USD: US weekly initial jobless claims; speech by St. Louis Fed President James Bullard

Friday, April 7

- USD: US March nonfarm payrolls (NFP)

- US and UK stock markets closed for Good Friday

Why is the NFP report important to global financial markets?

The US jobs report offers a major clue for how much higher the Federal Reserve can raise interest rates.

And various assets, including FX, commodities, and stocks, have been rocked by shifting forecasts surrounding the future rate adjustments by the world’s most influential central bank (the Fed).

Note that the Fed wants to see more “destruction” in the jobs market

While it’s odd to think that a central bank of the world’s largest economy would want to see more people losing their jobs (or at least fewer people getting jobs), but that’s the prescribed antidote by the Fed for subduing inflation that’s still too high.

Fewer people with jobs = less spending in the economy = businesses are less confident about hiking their prices aggressively = slower inflation

With the Fed already hiking US rates by 450 basis points over the past 12 months, here’s what markets are forecasting for the Fed’s next major adjustments to its benchmark interest rates:

-

60% chance of another 25 basis points hike in May 2023

-

61% chance of a 25-basis point cut in September

- 76% chance of the Fed lowering rates by a total of 50 basis points before 2023 is over

Those rate cuts by year-end are being priced in by the markets because they think the Fed won’t want to incur too much damage to the US economy and/or the financial system, especially after the recent turmoil in the US banking sector.

What are markets forecasting for the March NFP numbers?

-

Headline NFP number: 240,000 new jobs added in the US economy in March

-

Unemployment rate: 3.6%

- Average hourly earnings: 4.3% rise year-on-year (March 2023 vs. March 2022)

It’s important to note that the above forecasts set the base for how various assets may react (more on that later) to the official figures released a week from today.

Here are 2 broad potential outcomes from the upcoming NFP report:

-

A stronger-than-expected US jobs report may force markets into thinking that the Fed can afford to keep raising interest rates, provided it doesn’t incur more damage on the US banking sector.

- Further evidence of a weakening US jobs market (fewer jobs added/higher unemployment/slowing wage growth) may allow the Fed to pause its rate hikes, before eventually lowering them.

With all of the above in mind, here’s how these 3 assets are ready to react to the NFP prints:

1) USD Index

The US dollar tends to rise at the prospects of US interest rates moving even higher.

-

Stronger-than-expected US jobs report = higher bets for more Fed rate hikes in 2023 = USD index may retest its 50-day simple moving average (SMA) for resistance.

- Weaker-than-expected US jobs report = reinforce market bets for Fed rate cuts in 2023 = USD index may test the mid-January lows around 101.3 for support.

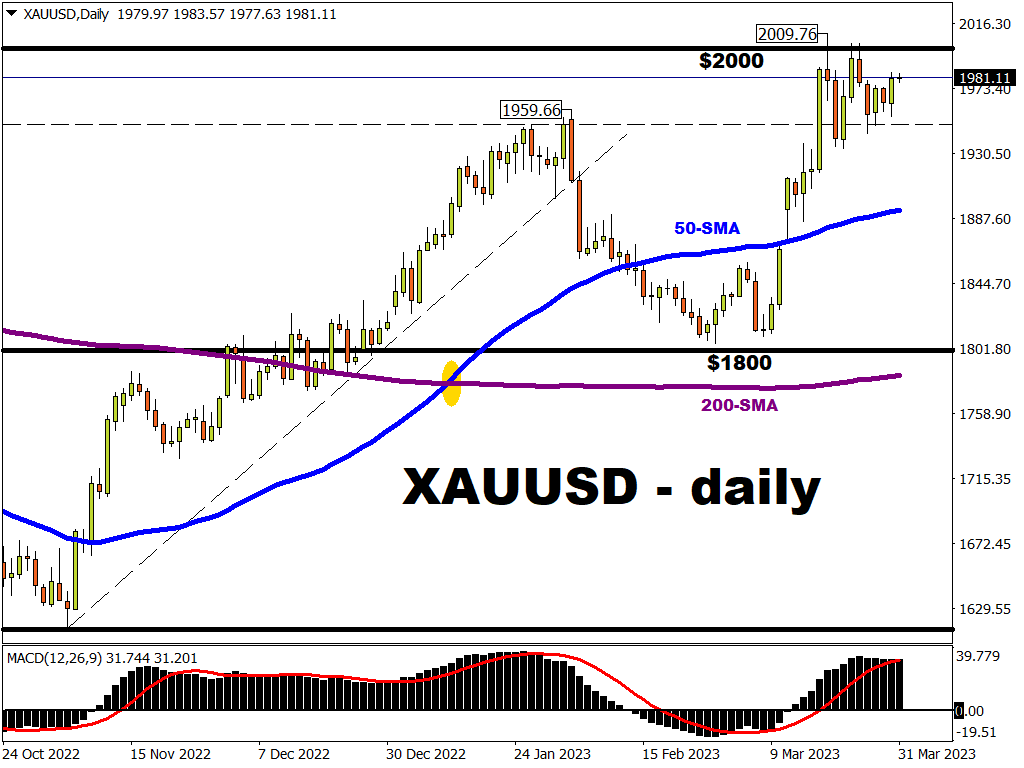

2) Gold

Note that gold is a zero-yielding asset, which means it does not pay interest to the investor for holding on to that asset.

Hence, the precious metal tends to fall at the thought of US interest rates moving higher, and vice versa.

-

Stronger-than-expected US jobs report = higher bets for more Fed rate hikes in 2023 = spot gold may drop back into sub-$1960 levels

- Weaker-than-expected US jobs report = reinforce market bets for Fed rate cuts in 2023 = gold may stay above the psychologically-important $2,000 mark.

3) NQ100_m

The Nasdaq 100 is an index that’s filled with US tech stocks, which generally do not like the thought of US interest rates moving higher.

-

Stronger-than-expected US jobs report = higher bets for more Fed rate hikes in 2023 = NQ100_m might falter back into sub-13,000 territory

- Weaker-than-expected US jobs report = reinforce market bets for Fed rate cuts in 2023 = NQ100_m might go above the late-August cycle high at 13,206.3.