After touching the year-to-date bottom from early February at 100.82 last week, the DXY has rebounded this week. If it holds onto its gains and prints a positive, green candle, that will at least stop a run of five consecutive weeks of losses. This has come about chiefly as US Treasury bond yields have also bounced back after a few weeks of turmoil brought on by the March banking madness / crisis.

The dollar recovery which began late last week follows a jump in US inflation expectations data. CPI figures around the globe, including yesterday’s hot UK numbers, have added to the theme that core inflation will stick around at higher levels for potentially longer than many market watchers believe. For the US, the all-important bond markets are seeing bets on interest rate cuts being priced out. The Fed funds rate is now seen at 4.6% by year-end, which is the highest since the banking turmoil began. This implies money markets are pricing in only two full cuts from the Fed’s peak by then. We note that there is only roughly a 20% chance of another 25bp rate hike beyond the FOMC’s May meeting.

All of this still indicates that the upside for the greenback remains limited as the Fed tightening cycle nears the end. The DXY is still just about in its bearish, descending channel from the March top at 105.88. Prices look like they need to advance above 102.80 at a minimum to arrest the downtrend.

Other major central banks on the move

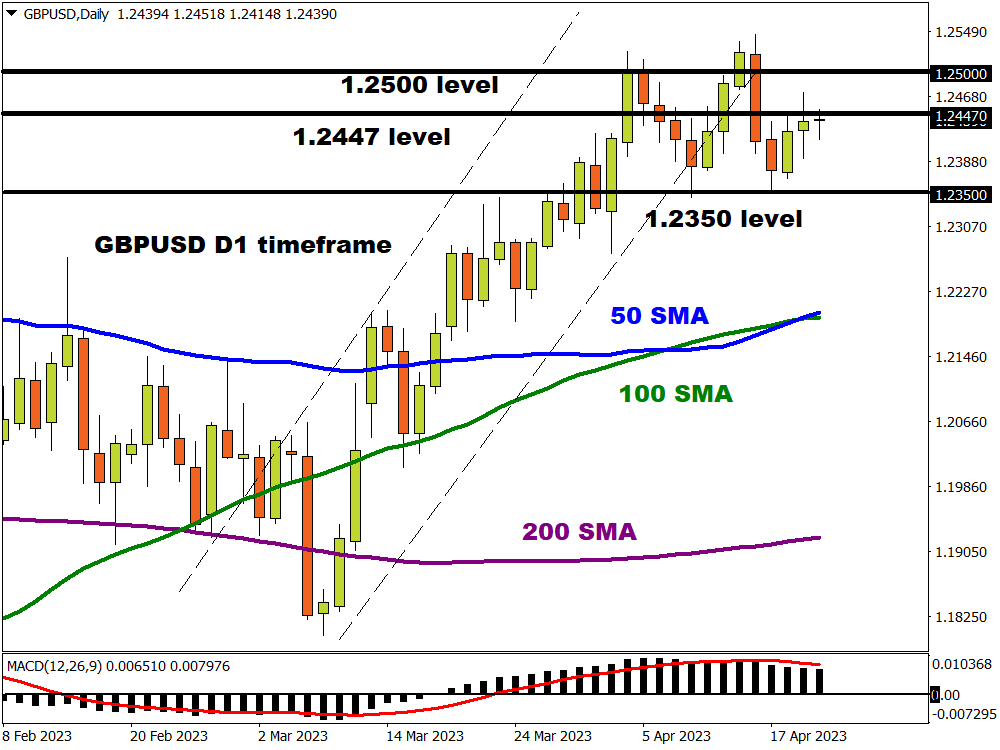

In contrast to the Fed, European central banks like the BoE, SNB and of course the ECB are seen as having more work to do to tame inflationary pressures. Strong UK data this week has rubber-stamped a 25bp rate hike at the Old Lady’s May meeting, the week after the FOMC and ECB rendezvous’. It has also seen another couple of rate rises priced in for MPC meetings into the summer. A peak UK rate of near 5% is the market bet though price action in the pound has been mixed this week. Support has been found on dips in GBP/USD with the mid-1.23s looking like solid support. But it is interesting we haven’t pushed higher towards 1.25, even with the solid data. A weekly close above the January top at 1.2447 would do nicely for the bulls.

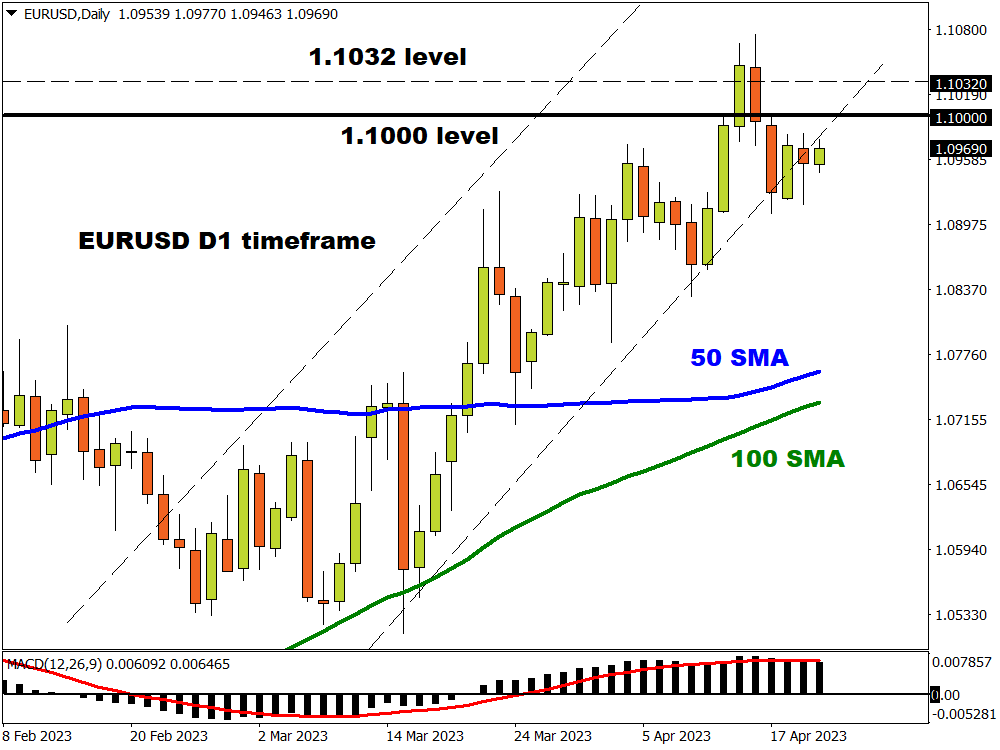

EUR still in its uptrend

Those elevated core prices are also sustaining market bets that the ECB will lift rates in the coming months. Again if we check out bond market which have been driving the wider market price action this year, the peak rate in the eurozone is seen around 3.87%, so a strong rebound from the 3% low priced during the heat of the banking maelstrom. In fact, it’s not that far away from the early March top just above 4%.

We get more ECB speakers on the wires today though it appears that the bar for a hawkish surprise is now high ahead of that huge week of central bank meetings in early May. Similar to GBP, the rise in rate hike bets hasn’t pushed EUR/USD to its recent highs, above 1.10. But dips have been supported and prices remain in an ascending channel with a series of higher highs and higher lows since early March. A weekly close above 1.1032 is important to sustain the bull trend.