The world's most-traded FX pair is attempting to pare some of yesterday's declines.

EURUSD's move higher at the time of writing is in spite of the just-released Eurozone inflation data for May, as measured by the consumer price index (CPI), arguing for greater declines for the bloc's currency.

-

6.1% rise compared to May 2022 (year-on-year), which is lower than the market's forecast of 6.3%, and also slower than April's 7% year-on-year figure.

-

Unchanged CPI (0%) month-on-month (May 2023 vs. April 2023), which is less than the market's forecasted 0.2% month-on-month rise, and also lower than April's 0.6% month-on-month rise (April 2023 vs. March 2023).

- Core CPI (excluding more volatile food and energy prices) rose 5.2% in May year-on-year, lower than the market's forecast of 5.5% and also lower than April's 5.6% year-on-year advance.

Traders largely ignored today's headline Eurozone inflation data, given that markets had already reacted to yesterday's (Wednesday, May 31st) inflation prints out of Germany and France - the Eurozone's two largest economies.

How does the Eurozone inflation data affect the Euro?

Generally, slower-than-expected inflation would lessen the need for the European Central Bank (ECB) to keep hiking its benchmark interest rate aggressively.

And a currency softens at the thought of interest rates not moving higher.

Markets expectations for those ECB interest rate adjustments have hardly shifted in recent weeks.

Markets still predict two more 25bp rate hikes by the ECB between now through September.

But the all-important difference between US and eurozone yields has widened recently and boosted the greenback, which in turn dragged EURUSD lower.

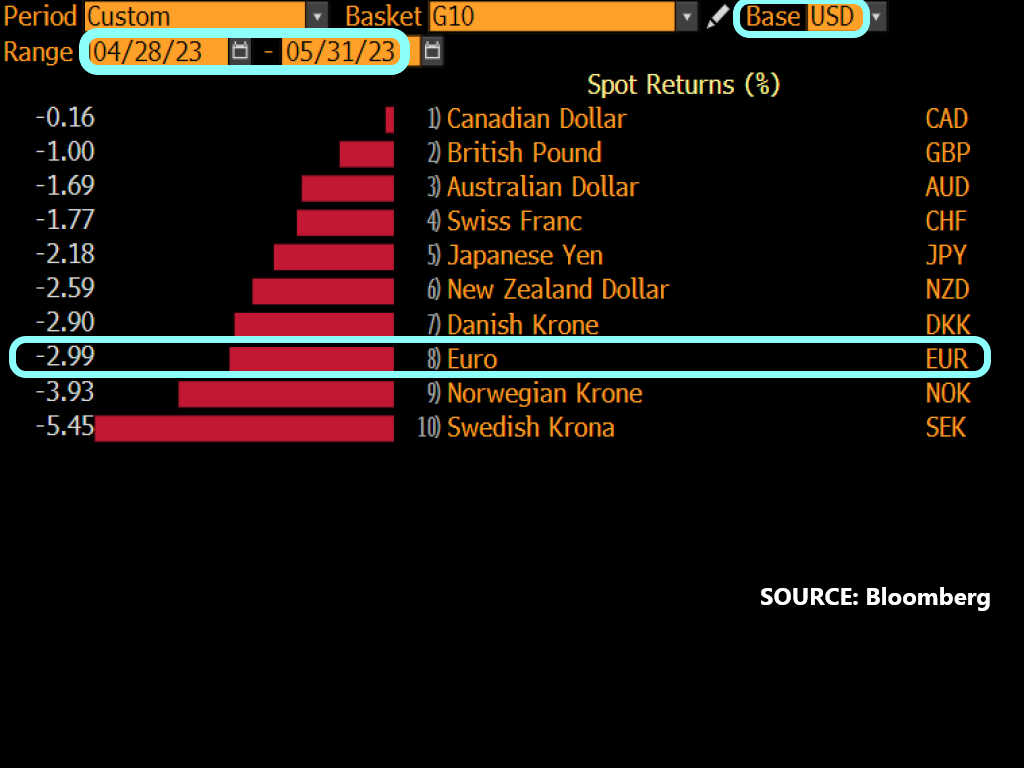

After all, the euro has already taken the brunt of the dollar buying with EUR/USD falling just shy of 3% last month.

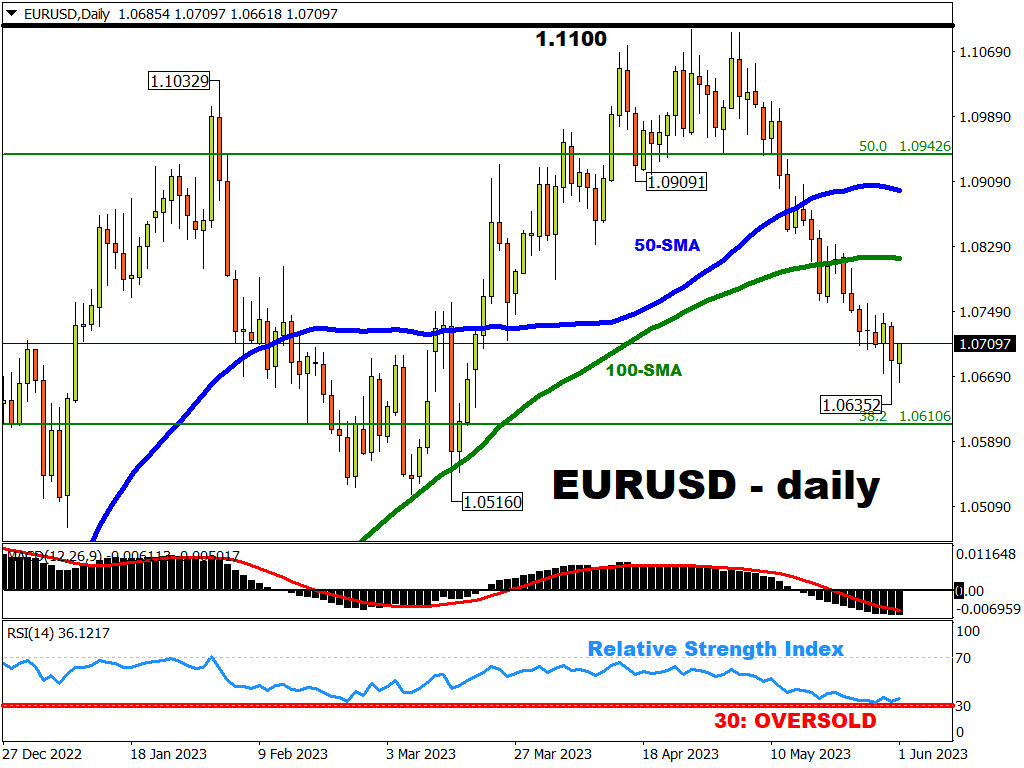

EUR/USD dropped to a ten-week low at 1.06352 yesterday before attempting to pare some of its losses at the time of writing.

A decisive loss of support around 1.07 could see more downside for the world’s most popular currency major.

The recent declines in EURUSD appears to have all but nullified the prospects for a rebound, as suggested in our latest Trade of the Week (published on Mondays).

But the week isn't over yet.

The remaining hope for a EURUSD rebound, albeit likely a limited one, rests on how Friday's US nonfarm payrolls report pans out:

- Economists are forecasting that 195,000 new jobs were added to the US economy in May, which would be its lowest tally since before the pandemic.

- Furthermore, the unemployment rate is expected to tick higher to 3.5%, relative to April’s 3.4% unemployment rate.

- Also, wage growth in May is expected to slow to 0.3% compared to April 2023 (month-on-month), which would be notably slower than April’s 0.5 month-on-month advance (compared to March 2023).

Potential scenarios:

- If there are more signs of slowing hiring momentum in the world's largest economy's labour market (lower-than-190k headline NFP number / higher-than-3.5% unemployment rate / lower-than 0.3% month-on-month wage growth), that could weaken the US dollar while offering relief for EURUSD.

Such a reaction would be based on the notion that a weakening US jobs market would lessen the need for the Fed to trigger another rate hike.

- However, the US dollar may strengthen and drag EURUSD lower if the US jobs market continues to demonstrate its resilience (higher-than-200k headline NFP number / lower-than-3.5% unemployment rate / higher-than 0.3% month-on-month wage growth)

A stronger-than-expected showing by the US jobs market may allow the Fed to hike once more this summer, if not in June then perhaps in July. And such prospects then likely to embolden dollar bulls.

When are markets expecting the next Fed rate hike?

The chances of a June hike according to futures markets had risen from less than zero at the start of May to nearly 60% on Tuesday (hence the US dollar's rebound).

However, those odds have been halved to around 35% at the time of writing.

But the idea that the FOMC will “skip” a June hike and hold rates steady in a couple of weeks’ time is gaining traction, and the idea has been backed up by recent Fedspeak, barring a sizzling red hot jobs report on Friday of course.

As long as markets are allowed to believe there's still one more Fed rate hike in the pipeline, that should keep the US dollar supported in the interim, while weighing on the rest of the FX universe.