Even as markets turn cautious ahead of the highly anticipated US jobs report later today (Friday, July 7), investors are bracing for more action in the week ahead thanks to another round of risk events.

It’s all about the incoming US inflation data, speeches from numerous Fed officials as well as earnings announcements by US banks which could inject fresh volatility into the S&P 500 over the coming week.

Monday, July 10

- CNH: China CPI, PPI

- GBP: Bank of England Governor Andrew Bailey speech

- USD: Fed speak - San Francisco Fed President Mary Daly, Cleveland Fed President Loretta Mester, Atlanta Fed President Raphael Bostic

Tuesday, July 11

- AUD: Australia consumer confidence

- EUR: Germany CPI & ZEW survey expectations

- GBP: UK jobless claims, unemployment report

- USD: St. Louis Fed President James Bullard speech

Wednesday, July 12

- CAD: Canada rate decision

- NZD: New Zealand rate decision

- JPY: Japan PPI

- USD: US June CPI report, Cleveland Fed President Loretta Mester, Atlanta Fed President Raphael Bostic speech

Thursday, July 13

- CNH: China trade

- EUR: Eurozone industrial production

- GBP: UK industrial production

- USD: US initial jobless claims, PPI

Friday, July 14

- JPY: Japan industrial production

- USD: University of Michigan consumer sentiment

- SPX500_m: Bank earnings - Wells Fargo, JP Morgan and Citigroup

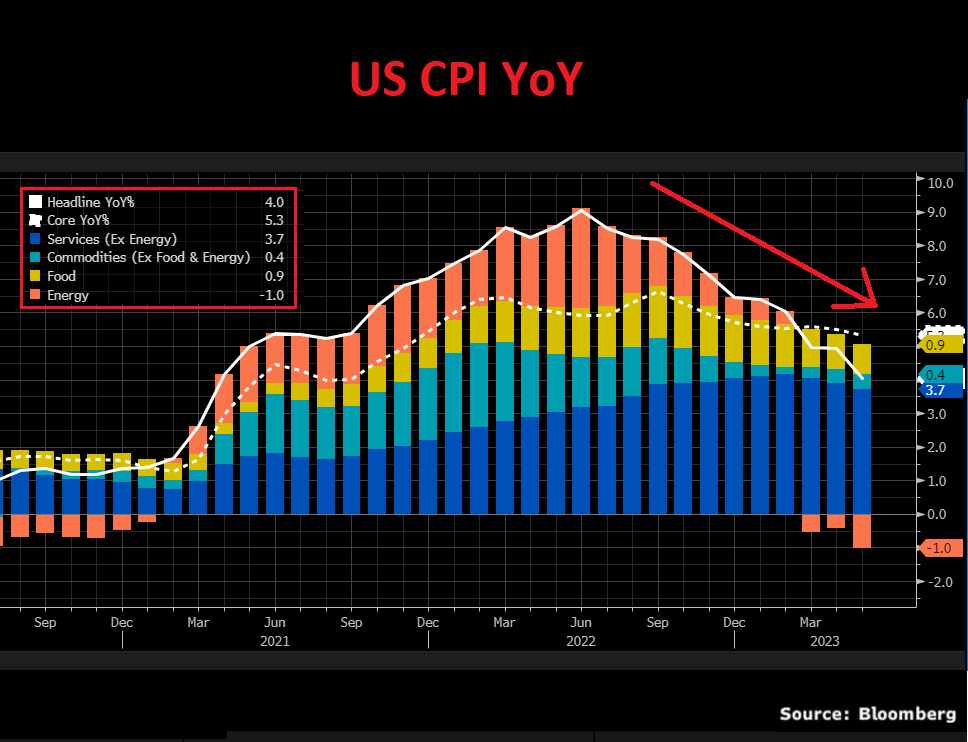

The June US Consumer price index (CPI) report published on Wednesday, July 12 will be one week after hawkish Fed minutes reinforced expectations around US rates staying higher for longer.

Given how the Fed remains data dependent, the strong ADP jobs report, pending NFP release this afternoon, and incoming US inflation data are likely to further influence Fed hike expectations.

Markets are forecasting:

- CPI year-on-year (June 2023 vs. June 2022) to cool 3.1% from 4.0% in the prior month.

- Core CPI year-on-year to cool 5.0% from 5.3% seen in May.

- CPI month-on-month (June 2023 vs May 2023) to rise 0.3% from 0.1% in the prior month.

- Core CPI month-on-month to cool 0.3% from 0.4% seen in May.

Over the past few months, there has been evidence of inflationary pressures cooling in the world’s largest economy, but core inflation has remained sticky. Should June’s CPI report slow further, this could fuel hopes around the Fed pausing rate hikes beyond July’s policy meeting.

How might the US CPI data influence the SPX500_m?

US equity bulls have warmly welcomed signs of cooling inflationary pressures as this supports the argument over the Fed pausing and eventually cutting interest rates down the road. Given how the S&P 500 Index has a handful of tech stocks that remain sensitive to Fed hike expectations, the CPI data could trigger volatility. In a nutshell, tech stocks dislike higher interest rates because their value is based on earnings projected in the future.

- The SPX500_m might find itself under renewed selling pressure if the inflation numbers exceed market expectations.

- Should the inflation numbers print below market forecasts, this could push the SPX500_m higher as expectations swell over the Fed nearing the end of its hiking cycle.

Let’s talk about US earnings season.

It’s that time of the year again!

Second quarter earnings season kicks off on Friday 14th July led by banking giants JP Morgan, Wells Fargo, and Citigroup. The bank earnings will be closely scrutinized for fresh insight into the US economy. It is worth keeping in mind that back in June, these major banks all passed the Fed’s stress test – lifting optimism ahead of earnings. Higher interest rates are expected to support bank earnings in the second quarter of 2023 as the Fed waged war against inflation.

Ultimately, a positive set of bank earnings may boost appetite for risk – injecting equity bulls with renewed confidence.

How might bank earnings impact the SPX500_m?

Given how financial stocks accounts for roughly 12.5% of the S&P 500, the market reaction to the earnings of these big banks on Friday could influence the index.

- The SPX500_m could push higher if the bank earnings exceed market expectations.

- If the earnings disappoint, the SPX500_m may trade lower.

Technical Outlook: Bulls vs Bears

The SPX500_m could be thrown on a roller-coaster ride next week if bulls and bears wrestle for control on the daily charts.

Even though prices are respecting a bullish channel on the D1 timeframe, bears are clearly in the vicinity and could ramp up their pressure if the index sinks back below 4332. Alternatively, bulls need to push prices beyond the 4463 resistance level to regain control of the steering wheel.

- A solid breakout above 4463 could encourage an incline towards 4500 and 4580, respectively.

- Should prices break down below 4332, this could encourage a decline to 4300, 4260, and 4200, respectively.