Asian markets were a mixed bag on Tuesday as weak China data countered the initial optimism set off by Wall Street overnight, after the benchmark S&P 500 notched its fifth consecutive monthly gain. European shares are flashing red amid the market caution with risk appetite taking another hit thanks to disappointing manufacturing activity data. Looking at currencies, the USD seems to be drawing strength from the tense mood while the Australian dollar has weakened across the board after the Reserve Bank of Australia left interest rates unchanged. Elsewhere, oil prices have slipped after bagging its biggest monthly gain since early 2022, while gold is wobbling around $1955 pressured by an appreciating buck.

Big week for the dollar

The greenback has kicked off the new month on a firm note, appreciating against every single G10 currency.

Dollar bulls seem to be drawing strength from cautious sentiment and a sense of anticipation ahead of some key data this week. Given the Federal Reserve's shift to data dependence, every US economic release moving forward will act as a key piece of information that may determine whether the Fed raises rates one final time in 2023 or not. This could translate to increased volatility for the US dollar over the next few months.

Focus will be directed towards the US ISM manufacturing report later today which has been in contractionary territory since November 2022. But the main risk event and potential market shaker will be the July nonfarm payrolls (NFP) on Friday. Ultimately, a weaker-than-expected jobs report could support the argument around the Fed being done with raising rates in 2023.

Currency spotlight – GBPUSD

Sterling may experience heightened volatility this week due to the Bank of England rate decision on Thursday. Given how the decision will be accompanied by the quarterly Monetary Policy Report (MPR), this Super Thursday combo could send GBPUSD on a roller coaster ride. Markets widely expect the BoE to raise interest rates by 25bp in the face of sticky inflation. However, recession fears remain elevated amid disappointing data, and this could offer support to the doves on the MPC. Should the central bank surprise markets with a 50bp hike, this could send the British Pound surging across the board.

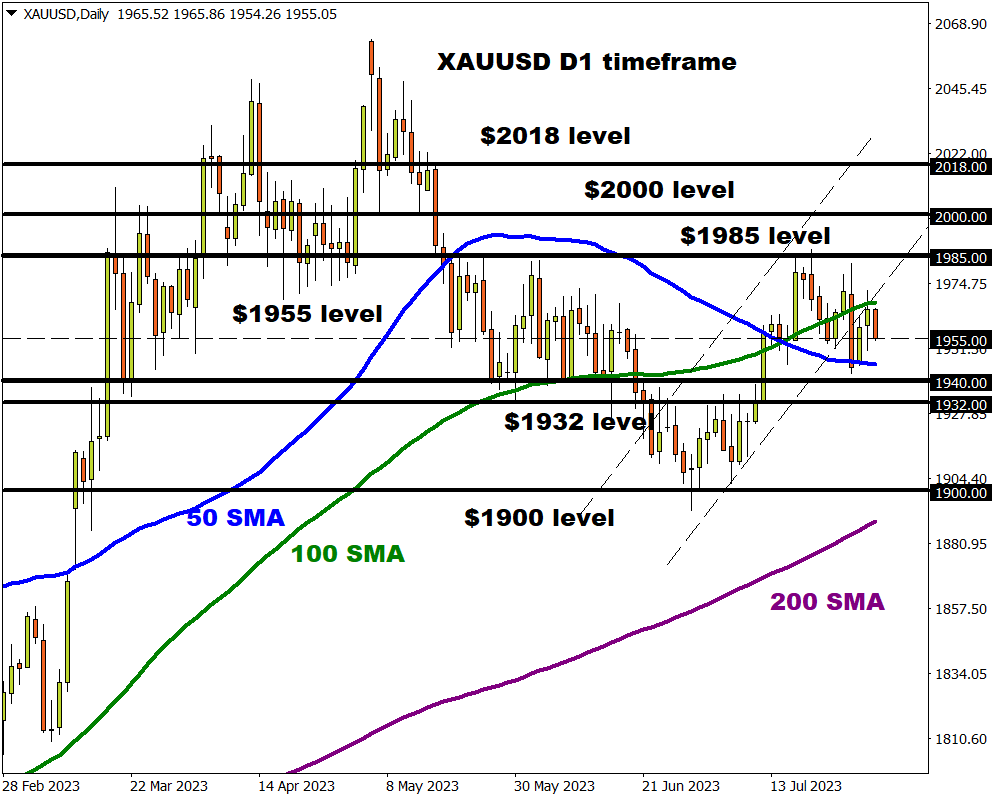

Commodity Spotlight – Gold

The Fed’s shift to data dependence may translate to heightened volatility for gold, with the precious metal poised to display increased sensitivity to Friday’s NFP report.

Given how markets are only pricing in a 19% probability of a rate hike in September with this jumping to 37% by November, gold bulls remain in a comfortable position. However, September's Fed meeting is just less than two months away which is enough time for much to happen.

Nevertheless, the path of least resistance for gold points north with a disappointing jobs report on Friday potentially opening a path back toward $1985. A solid breakout above this point could open the doors toward the psychological $2000 level. Should prices slip back below the 50-day SMA, a decline toward $1940 and $1932 could be on the cards.