-

Final week of Q3 2023 may prove relatively less hectic for markets

-

EURUSD still set to uncover trading opportunities

-

Eurozone data may point to even-darker economic outlook

-

US dollar could be boosted by PCE Deflators, hawkish Fed speak

- Bloomberg model: 74% chance EURUSD trades within 1.0542 – 1.0770

Managed to catch your breath yet after such a hectic week in the markets?

At least the coming ahead may prove to be less eventful in comparison, providing a relative breather before we enter the final quarter of 2023.

Still, EURUSD traders are bound to discover fresh trading opportunities in the week ahead.

Key data releases from either side of the Atlantic should move the world’s most-traded FX pair.

But first, here’s a quick list of major events and data releases due in the final week of September:

Monday, September 25

- EUR: Germany IFO business climate (Sept)

- USD: Speech by Minneapolis Fed President Neel Kashkari

Tuesday, September 26

- EUR: Speeches by ECB’s Robert Holzmann, Philip Lane

- USD: US consumer confidence (Sept)

Wednesday, September 27

- JPY: Bank of Japan meeting minutes

- CNH: China industrial profits (Aug)

- EUR: Germany consumer confidence (Oct)

Thursday, September 28

- AUD: Australia retail sales (Aug)

- EUR: Germany CPI (Sept); Eurozone economic and consumer confidence (Sept)

- USD: US weekly initial jobless claims; 3Q GDP (3rd estimate)

- USD: Speeches by Fed Chair Jerome Powell, Richmond Fed President Tom Barkin; Chicago Fed President Austan Goolsbee

- Nike quarterly earnings

Friday, September 29

- JPY: Tokyo CPI (Sept); jobless rate, industrial production, and retail sales (Aug)

- GBP: UK 2Q GDP (final)

- EUR: Eurozone CPI (Sept); Germany unemployment (Sept)

- USD: US PCE deflator, consumer spending (Aug); speech by New York Fed President John Williams

Data to show still-gloomy Eurozone economy?

Markets have of late been growing more concerned about the Eurozone’s economic prospects.

After all, Germany, the largest economy in the bloc, is widely expected to see its economy shrink for 2023.

And that’s according to economists, the OECD, and even the Bundesbank – Germany’s own central bank.

Amid such a darkening economic outlook, comes also the fact that the Eurozone’s consumer price index (CPI) – which measures headline inflation – remains more than twice the European Central Bank’s 2% target.

The above combo (economic woes + stick inflation) is set to bind the hands of ECB hawks (policymakers who want to send interest rates higher) from triggering yet another rate hike.

At the time of writing, markets are pricing in a mere 24% chance that the ECB can trigger one final 25-basis point hike by January 2024.

To oversimplify …

Greater economic woes = ECB unable to hike, despite sticky inflation = lower EURUSD

Then, on the USD side of the equation …

Fed speak, US data to offer clues on last Fed rate hike

Several Fed officials, including Fed Chair Jerome Powell, are due to make public speeches in the week ahead.

Such commentary comes hot on the heels after this week’s FOMC meeting (Sept 19-20th), which concluded with Chair Powell pressing home the “higher-for-longer” message.

That is to say, the US central bank is expecting to:

-

hike by another 25-basis points before end-2023 (markets are predicting a 53% chance for one more Fed rate hike by December)

-

keep US interest rates at their peak above 5% for a longer-than-previously expected length of time

- lower their benchmark rates by “only” 50 basis points in 2024, which is half of the 100-bps in rate cuts previously forecasted by FOMC officials (via their “dot plot) back in June.

Set against such expectations, Powell and co. may be looking to further impress their hawkish messaging onto traders and investors worldwide in this final week of September.

As things stand, existing expectations for the Fed’s policy settings have already lifted the benchmark US dollar index to its highest levels since March.

NOTE: The Euro accounts for 57.6% of this US dollar index, which measures how the greenback performs against a basket of major peers, including the Japanese Yen, British Pound, Canadian Dollar, Swedish Krona, and Swiss Franc.

Also look out for Friday’s release (Sept 29th) of the Fed’s preferred measure of inflation, the PCE Deflator.

That set of data is expected to show a mixed picture, based on current forecasts by economists:

-

PCE Deflator month-on-month (Aug 2023 vs. July 2023): 0.5% estimate.

If so, that would be higher than July’s 0.2% month-on-month number

-

PCE Deflator year-on-year (Aug 2023 vs. Aug 2022): 3.5% estimate.

If so, that would be higher than July’s 3.3% year-on-year number

-

PCE Core Deflator month-on-month: 0.2% estimate.

If so, that would match July’s 0.2% month-on-month number

- PCE Core Deflator year-on-year: 3.9% estimate.

If so, that would be lower than July’s 4.2% year-on-year number

POTENTIAL SCENARIOS

-

EURUSD may be dragged to a fresh 6-month low if the coming week’s data out of Germany/Eurozone further sours the bloc’s economic outlook and narrows the ECB’s chances at one last rate hike in this cycle, while the US PCE Deflators and Fed speak strengthen the case for one final Fed rate hike in this cycle.

- EURUSD may be offered relief and move back higher on better-than-expected economic data out of the Eurozone/Germany, while the US PCE Deflators come in below forecasts which dilute the case for one final Fed rate hike in this cycle.

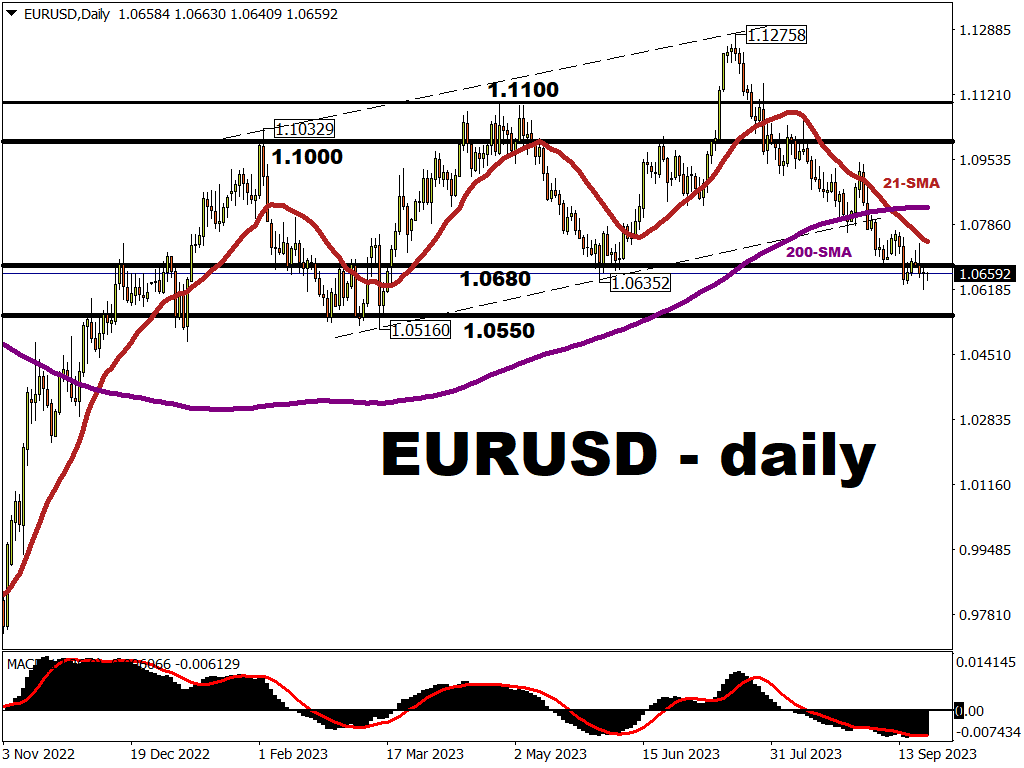

Key levels

At the time of writing, Bloomberg’s FX model points to a 74% chance that EURUSD will trade within the 1.0542 – 1.0770 range over the next one-week period.

Here are some notable price levels within that range for further consideration:

POTENTIAL RESISTANCE

-

1.06800: support turned resistance level since Dec 2022

-

1.07369: intraday high on Sept 20th, also around 21-day simple moving average (SMA)

-

1.07700: upper bound of Bloomberg’s FX model

POTENTIAL SUPPORT

-

1.06170: intraday low on Sept 21st

-

1.06000: psychologically-important level

- 1.05160 - 1.0542: price region between Q1 2023 intraday low and lower bound of Bloomberg model forecasted range