The USDJPY has kicked off the new trading week by touching its highest level since November 2022.

Yen bears are clearly in power, with the Japanese yen currently the worst performing G10 currency year-to-date, shedding roughly 11.8% against the dollar.

Last Friday, the Bank of Japan (BoJ) left its ultra-loose monetary policy unchanged and kept its dovish stance despite high inflation. While the policy divergence between the Fed and BoJ remains a key driving force behind the USDJPY’s upside, the threat of government intervention could frighten bulls down the road.

Taking a trip down memory lane, the BoJ intervened back in September 2022 when the yen weakened to 145.90. Two more interventions followed in October after the Yen fell below 150.

Given how the currency is weaker than last year when Japan acted, investors remain on high alert with much chatter around 150 acting as a key level that could trigger government intervention.

It is worth keeping in mind that a weakening Yen results in higher import prices. This is transferred to producers, boosting expectations for higher inflation with consumers feeling the pain. Such a development could be a headache for policymakers, especially when factoring in how Japan’s headline and core inflation remain above the BOJ’s 2% target.

With all the above said, the threat of government intervention has made the USDJPY a ticking timebomb that could explode at any moment…

Here are 3 factors that could impact the currency pair this week:

-

Fed speeches + US August PCE report

A host of Fed officials, including Fed Chair Jerome Powell will be under the spotlight this week.

Last week’s FOMC meeting concluded with Powell indicating that rates will remain “higher for longer”. Should policymakers strike a hawkish tone and reinforce last week’s messaging, the USDJPY could push higher as expectations rise around the Fed hiking rates once more hike in 2023.

Regarding the August PCE report, markets expect the August PCE report to show headline prices accelerated 0.5% month-over-month after July’s 0.2% increase while the core PCE deflator is forecast to rise 0.2%, same as July. The core personal consumption expenditures price index for projected to rise 3.9% year-over-year in August, down from the 4.2% seen in July.

Ultimately, more signs of cooling inflationary pressures may counteract the argument around the Fed “keeping rates higher for longer”, weakening the USDJPY as a result.

-

Japan data dump

Investors will be dished out some key economic reports from Japan on Friday.

All eyes will be on the Tokyo inflation data for September, jobless rate, industrial production, and retail sales figures for August which could provide insight into the health of Japan’s economy.

- Should the overall economic data from Japan print above market expectations, this may boost sentiment towards the Japanese economy – pulling the USDJPY lower as the yen strengthens.

- If overall economic data disappoints, sentiment toward the Japanese economy could take a hit – pushing the USDJPY higher as the yen weakens.

-

Technical forces

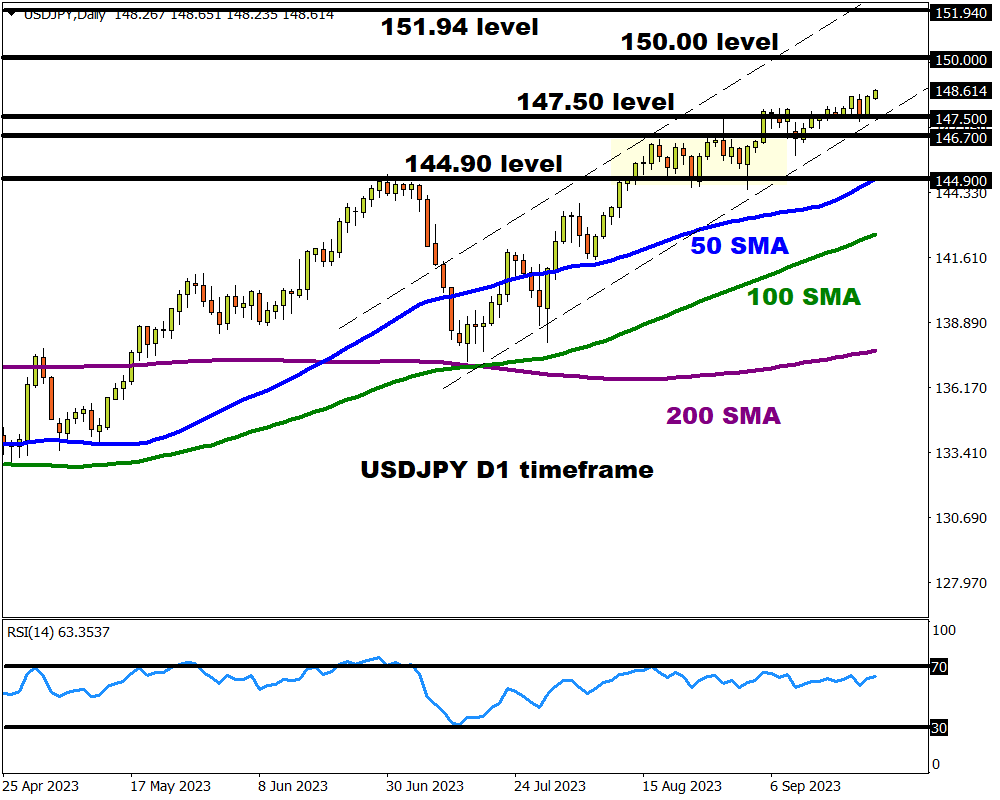

The USDJPY is firmly bullish on the daily timeframe as there have been consistently higher highs and higher lows. However, prices are slowly approaching overbought conditions while bulls displaying slight hesitation due to key fundamental forces.

- The current upside could take prices towards the 150.00 psychological level. Beyond this point, the next key level of interest is the 2022 high at 151.94.

- Should bulls get cold amid intervention fears, prices could slip back below 147.50, 146.70, and 144.90, respectively.