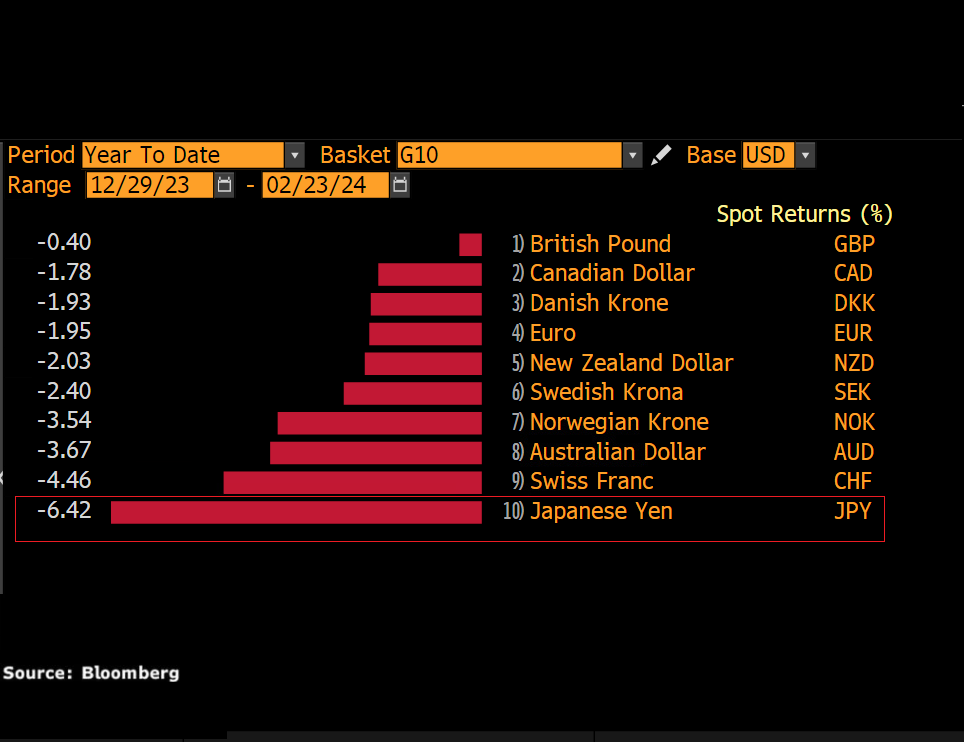

- JPY worst performing G10 YTD

- Japan CPI & US PCE in focus

- Yen back on intervention watch

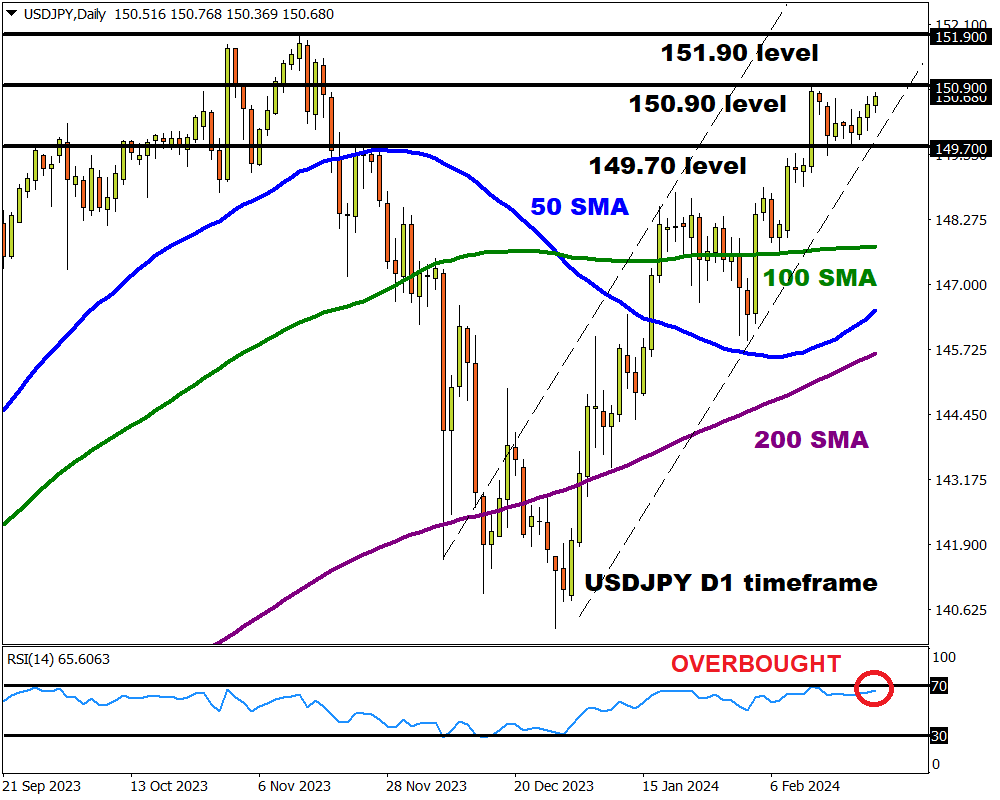

- Prices bullish but RSI overbought

- Key level of interest at 150.90

Our focus lands on the Japanese Yen which has been the worst-performing G10 currency against the US Dollar year-to-date.

The final trading week of February promises to be eventful due to key economic data, speeches by numerous Fed officials, and threat of a partial US government shutdown:

Tuesday, 27th February

- JPY: Japan CPI

- GBP: BOE Governor Andrew Bailey speech

Wednesday, 28th February

- EUR: Eurozone economic confidence, consumer confidence

- NZD: New Zealand rate decision

- USD: Q4 GDP (2nd estimate), Atlanta Fed President Raphael Bostic, Boston Fed President Susan Collins, New York Fed President John Williams speech

Thursday, 29th February

- AUD: Australia retail sales

- CAD: Canada GDP

- EUR: Germany CPI, unemployment

- JPY: Japan industrial production, retail sales

- USD: US January PCE report, Chicago Fed President Austan Goolsbee, Atlanta Fed President Raphael Bostic, Cleveland Fed President Loretta Mester speech

Friday, 1st March

- CNH: China official PMI, Caixin manufacturing PMI

- EUR: Eurozone CPI, unemployment, PMI, Germany Manufacturing PMI

- GBP: UK S&P Global/CPIS Manufacturing PMI

- USD: US ISM manufacturing, University of Michigan consumer sentiment, Fed speeches

- Deadline for avoiding partial US government shutdown

Yen weakness has been a major theme this quarter thanks to a dovish BoJ, with the recession in Japan fuelling uncertainty about likely timings for a policy pivot.

Note: Yen down more than 6% versus the USD year-to-date.

The Yen’s recent depreciation below 150 per dollar has sparked warnings from Japanese officials, ultimately fuelling market fears of possible intervention.

With the USDJPY venturing closer to multi-year highs just below 152, a major move could be brewing.

With all the above said, here are 3 factors that could influence the USDJPY:

-

Japan inflation data

Japan’s national consumer price index (CPI) is forecast to slow to 1.9% year on year in January from the 2.6% in January. The core measure which excludes fresh food is expected to cool 1.9% year on year, down from 2.3% in December.

Should expectations match reality, this will be the first time the core CPI has dipped below the BoJ’s 2% target since March 2022.

Traders are currently pricing in only a 29% probability that the BoJ will scrap negative rates by March, with the odds jumping to 78% by April.

- A softer than expected inflation report may support the argument around the economy being too weak for rate hikes, weakening the Yen as a result.

- Should the inflation report print above expectations, this could boost the Yen as expectations mount over the BoJ ending negative rates.

-

US January PCE report

The Fed’s preferred inflation gauge – the Core Personal Consumption Expenditure is likely to influence rate cut expectations.

Traders are currently pricing in 79% probability of Fed rate cut by June, according to Fed fund futures.

The PCE core deflator is forecast to rise 0.4% month-over-month, from 0.2% in December while cooling 2.8% in January, down from 2.9% in the previous month.

- Ultimately, more signs of cooling price pressures may boost bets around the Fed cutting interest rates down the road – hitting the dollar as a result.

- If the PCE report prints above market forecasts, this could further dampen hopes for early rate cuts – pushing the USDJPY higher as a result.

Note: Looking beyond the PCE report and other key US data, it may be wise to keep an eye on the looming partial government shutdown.

The United States is facing another partial government shutdown deadline set to expire on 1st March. Should this become reality, it could impact the dollar and risk sentiment – reflecting on the USDJPY.

-

Technical forces

The USDJPY is firmly bullish on the daily timeframe as there have been consistently higher highs and higher lows. However, the Relative Strength Index (RSI) is approaching 70 – signalling that prices are overbought.

- A solid weekly close above 150.90 may encourage an incline towards the 151.90 level.

- Should bulls get cold feet below 150.90, this may trigger a selloff towards 149.70 and potentially lower.