- Tokyo CPI & US PCE in focus

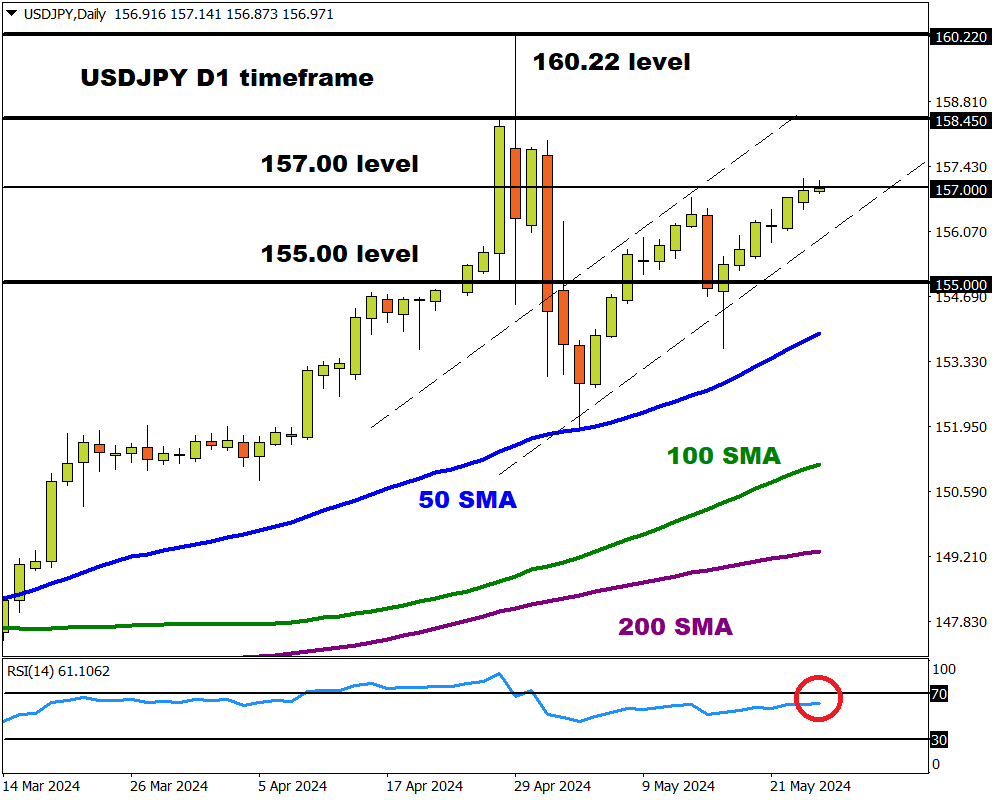

- USDJPY 2% away from multi-decade top

- Prices bullish but RSI near overbought

- Bloomberg FX model – 77% USDJPY – (155.21 – 158.45)

Despite the holiday-shortened week ahead for the UK and US, markets could remain volatile due to top-tier data across the globe:

Monday, 27th May

- UK and US markets closed

- CN50: China industrial production

- GER40: Germany IFO business climate

- EU50: ECB chief economist Philip Lane speech

Tuesday, 28th May

- AU200: Australia retail sales

- US30: US Conference Board consumer confidence, Fed speech

Wednesday, 29th May

- GER40: Germany CPI

- ZAR: South African election

- US500: Fed Beige Book, New York Fed President John Williams speech

Thursday, 30th May

- EU50: Eurozone economic confidence, unemployment

- ZAR: South Africa rate decision

- SEK: Sweden GDP

- CHF: Switzerland GDP

- TWN: Taiwan GDP

- US500: US initial jobless claims, GDP (Second Est), Fed speech

Friday, 31st May

- CAD: Canada quarterly GDP

- CN50: China official PMI’s

- EUR: Eurozone CPI

- JPY: Japan unemployment, Tokyo CPI, industrial production, retail sales

- USDInd: US May PCE report, Atlanta Fed President Raphael Bostic speech

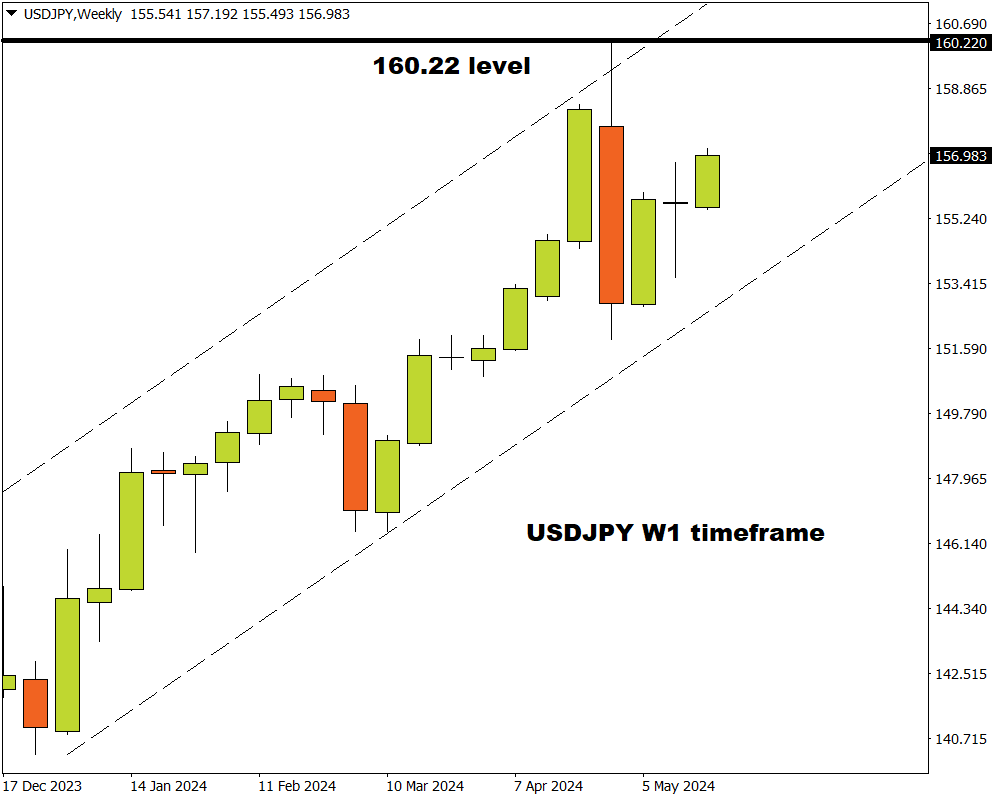

A few weeks ago, the yen was a hot talking point after staging a dramatic reversal against the dollar. This development fueled speculation about possible intervention by Japanese authorities after the currency weakened to a 34-year low.

Fast forward to today, the yen has given back most of its gains and is currently trading 2% away from its multi-decade top. Could another intervention be on the horizon if prices retest the 160.22 level?

The USDJPY could end May with a bang, and here are 3 reasons why:

1) Japan data dump

Incoming data from Japan could inject the yen with fresh volatility.

Much focus will be directed towards the latest CPI figures from Tokyo, unemployment, industrial production, and retail sales for insight into the health of Japan’s economy. This data dump may also influence expectations around when the Bank of Japan will proceed with another rate hike.

Traders are currently pricing in only a 27% probability of a 10-basis point hike by June with this jumping to 88% by July.

- Should overall data support expectations around the BoJ hiking rates further, this could boost the yen.

- A disappointing set of data that tempers bets around higher rates in Japan could weaken the yen.

2) US April PCE report

The Fed’s preferred inflation gauge - the Core Personal Consumption Expenditure is likely to influence rate cut expectations.

Recent data from the United States have eroded bets around the Fed cutting rates anytime soon.

Traders are pricing in a 60% probability of a 25-basis point cut by September with this jumping to 87% by November.

The PCE core deflator is forecast to remain unchanged at 0.3% month-over-month, with the same expected for its year-on-year print at 2.8%.

- More signs of cooling price pressures may rekindle Fed cut bets, dragging the USDJPY lower as a result.

- If the PCE report prints above market forecasts, this could support the “higher for longer” narrative – pushing the USDJPY higher as a result.

Note: Looking beyond the US PCE report, it will be wise to keep an eye on speeches by numerous Fed officials and other key US data points that may influence the dollar.

3) Technical forces

The USDJPY is trending higher on the daily timeframe as there have been consistently higher highs and higher lows. However, the Relative Strength Index is slowly approaching 70 – indicating that prices may be nearing overbought conditions.

- A solid breakout and daily close above 157.00 may open a path back towards 158.45.

- Should 157.00 prove to be reliable resistance, this may encourage a decline back towards 155.00.