Major central banks may further adjust monetary policy in 2025 as the European Central Bank (ECB) insists that ‘the disinflation process is well on track,’ but the Federal Reserve may change gears at a slower pace as Chairman Jerome Powell and Co. forecast less rate-cuts for next year.

North America

Federal Reserve

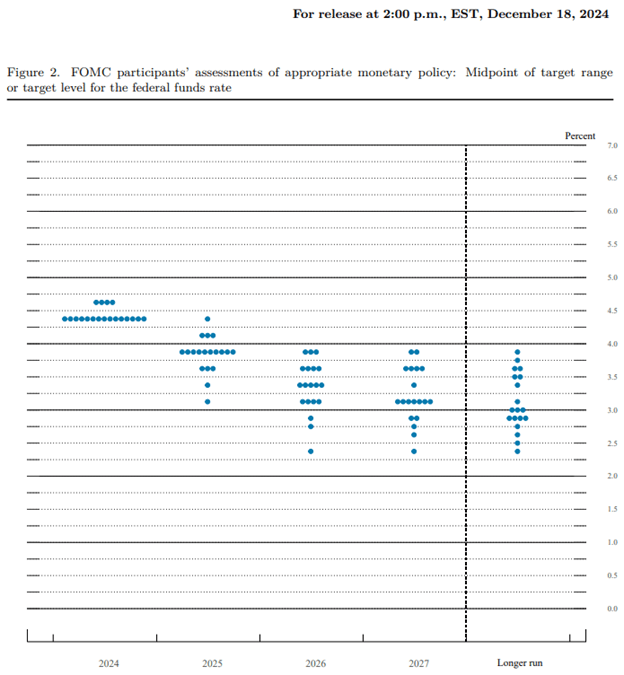

The Federal Open Market Committee (FOMC) acknowledged that ‘our policy stance is now significantly less restrictive’ after lowering US interest rates by another 25bp at its last meeting for 2024, with the central bank going onto say that ‘we can therefore be more cautious as we consider further adjustments to our policy rate.’

Source: FOMC

It seems as though the FOMC will say on track to further unwind its restrictive policy in 2025, but the committee may continue to adjust its forward guidance as the update to the Summary of Economic Projections (SEP) shows that ‘the median participant projects that the appropriate level of the federal funds rate will be 3.9% at the end of next year’ compared to the 3.4% forecast at the September meeting.

In turn, speculation surrounding Fed policy may continue to sway foreign exchange markets as Chairman Powell and Co. insist that ‘monetary policy will adjust in order to best promote our maximum employment and price stability goals,’ and the US Dollar may outperform against its major counterparts in 2025 should the FOMC show a greater willingness to further combat inflation.

Europe

European Central Bank

The European Central Bank (ECB) lowered Euro Area interest rates by 25bp in December, and the Governing Council may continue to shift gears in 2025 as ‘most measures of underlying inflation suggest that inflation will settle at around our two per cent medium-term target on a sustained basis.’

It seems as though the ECB will stick to its rate-cutting cycle as the ‘staff now expect a slower economic recovery than in the September projections,’ and the Governing Council may unwind its restrictive policy at a faster pace as President Christine Lagarde reveals that ‘there were some discussions, with some proposals to consider possibly 50 basis points.’

As a result, the Governing Council may sound increasingly dovish in 2025 as ‘underlying inflation is overall developing in line with a sustained return of inflation to target,’ and it remains to be seen if the ECB will reach its neutral rate ahead of its US counterpart amid the upward revision in the Fed’s interest rate dot-plot.

EUR/USD Weekly Chart

Source: TradingView

Keep in mind, EUR/USD continues to hold below pre-US election rates after registering a fresh yearly low (1.0333) in November, and a weekly close below the 1.0370 (38.2% Fibonacci extension) to 1.0410 (50% Fibonacci retracement) region may push the exchange rate towards 1.0200 (61.8% Fibonacci retracement).

Next area of interest comes in around 0.9910 (78.6% Fibonacci retracement) to 0.9950 (50% Fibonacci extension), but EUR/USD may track the flattening slope in the 50-Week SMA (1.0824) if it continues to hold above 1.0200 (61.8% Fibonacci retracement).

Need a weekly close above 1.0610 (38.2% Fibonacci retracement) to bring the 1.0870 (23.6% Fibonacci retracement) to 1.0940 (50% Fibonacci retracement) zone on the radar, with the next region of interest coming in around 1.1070 (23.6% Fibonacci retracement) to 1.1090 (38.2% Fibonacci extension).

Asia/Pacific

Bank of Japan

Meanwhile, the Bank of Japan (BoJ) voted 8 to 1 to keep the benchmark interest rate around 0.25% in December, and the central bank may retain the current policy over the coming months as ‘underlying CPI inflation is expected to increase gradually.’

As a result, the Japanese Yen may continue to service as a funding-currency as the BoJ remains reluctant to pursue a rate-hike cycle, but Governor Kazuo Ueda and Co. may come under pressure to implement higher interest rates as ‘Japan's economy is likely to keep growing at a pace above its potential growth rate.’

With that said, the carry-trade may further unwind in 2025 should the BoJ adopt a hawkish guidance, and the Japanese Yen may face increases volatility over the coming months as major central banks continue to change gears.

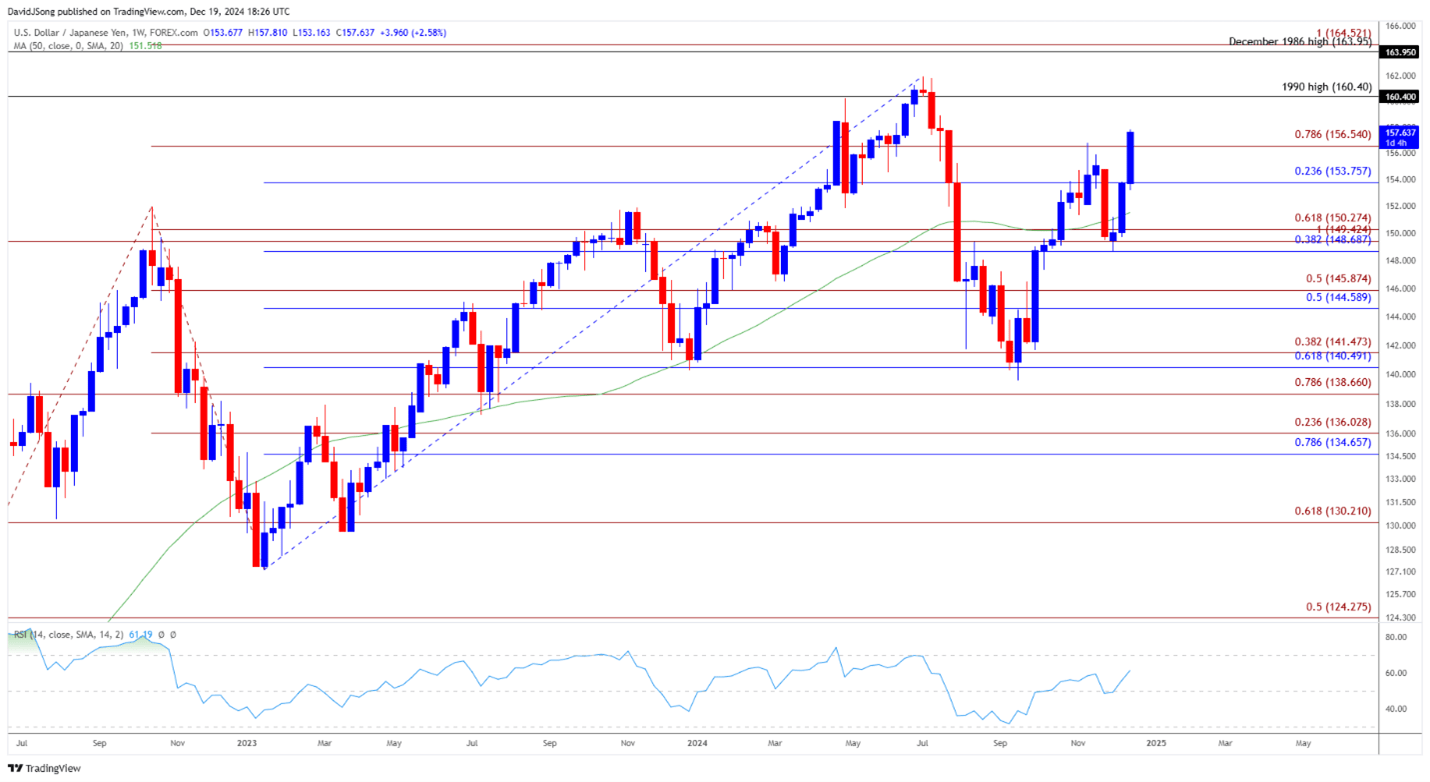

USD/JPY Weekly Chart

Source: TradingView

USD/JPY trades back above pre-US election rates as it pushes above the November high (156.75), with a breach above 160.40 (1990 high) opening up the 2024 high (161.95).

Next region of interest comes in around the December 1986 high (163.95), but lack of momentum to close above 160.40 (1990 high) on a weekly basis may keep USD/JPY within the 2024 range.

Need a weekly close below 156.50 (78.6% Fibonacci extension) to bring 153.80 (23.6% Fibonacci retracement) on the radar, with the next area of interest coming in around 148.70 (38.2% Fibonacci retracement) to 150.30 (61.8% Fibonacci extension).