The FX world could see some heightened volatility if the US Dollar receives a double boost, along with any surprises out of G10 central banks in action over the coming week:

Monday, March 6

- AUD: Australia February inflation gauge

- EUR: Euro area January retail sales

Tuesday, March 7

- AUD: Reserve Bank of Australia decision; Australia January external trade

- CNH: China February external trade

- EUR Germany January factory orders

- USD: Fed Chair Jerome Powell testifies before Congress

Wednesday, March 8

- AUD: RBA Governor Philip Lowe speech

- EUR: Eurozone 4Q GDP (final); Germany January industrial production and retail sales; ECB President Christine Lagarde speech

- US crude: EIA crude oil inventories

- CAD: Bank of Canada rate decision

- USD: Fed Chair Jerome Powell continues testimony before Congress

Thursday, March 9

- JPY: Japan 4Q GDP (final)

- CNH: China February CPI

- USD: US weekly jobless claims; US President Joe Biden to release fiscal 2024 US budget

Friday, March 10

- JPY: Bank of Japan rate decision; Japan February PPI

- EUR: Germany February CPI (final)

- GBP: UK January GDP, industrial production, and trade balance

- CAD: Canada February jobs report

- USD: US February nonfarm payrolls report

Of course, we must start with King Dollar, which is set to face two major catalysts:

Fed Chair Powell’s 2-day testimony before Congress (March 7-8)

The US dollar may climb higher if the boss of the world’s most influential central bank affirms that US interest rates have to be raised further in order to vanquish red-hot inflation.

February US jobs report (Friday, March 10)

Here are the forecasts for this widely-followed economic data:

- Nonfarm payrolls: 215,000 (lower than January’s blockbuster 517,000 new jobs added)

- Unemployment rate: 3.4% (matching pre-pandemic lows)

- Average hourly earnings month-on-month growth: 0.3% (matching January’s 0.3% month-on-month growth)

The US dollar could grow stronger if the above data exceed market forecasts, especially if still-resilient US hiring along with faster earnings growth feed into inflationary pressures.

Still-stubborn inflation would then force the Fed into prolonging its policy tightening, despite already triggering 450 basis points in demand-destroying rate hikes.

And recall that currencies tend to be boosted by the prospects of its economy’s interest rates moving even higher than its peers.

Fed Chair Powell pressing home his hawkish policy bias + US jobs report exceeds market expectations = double boost for Dollar bulls!

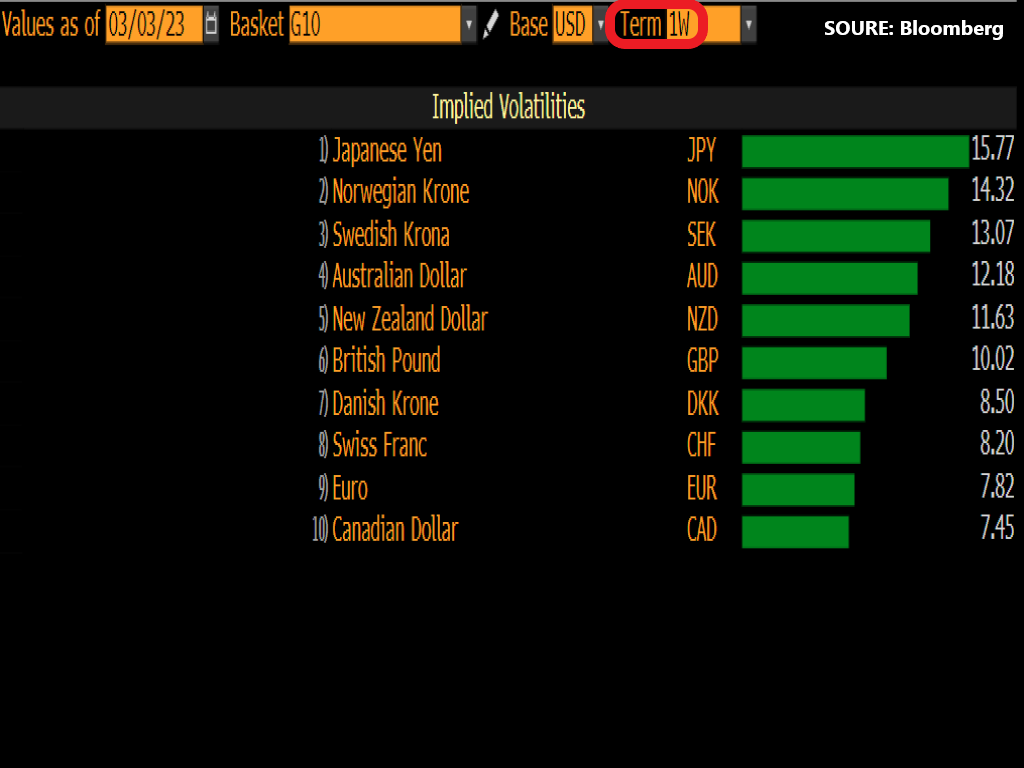

Moving beyond the USD side of the FX equation, here are three G10 FX pairs that’s set for an eventful week ahead:

1) USDJPY

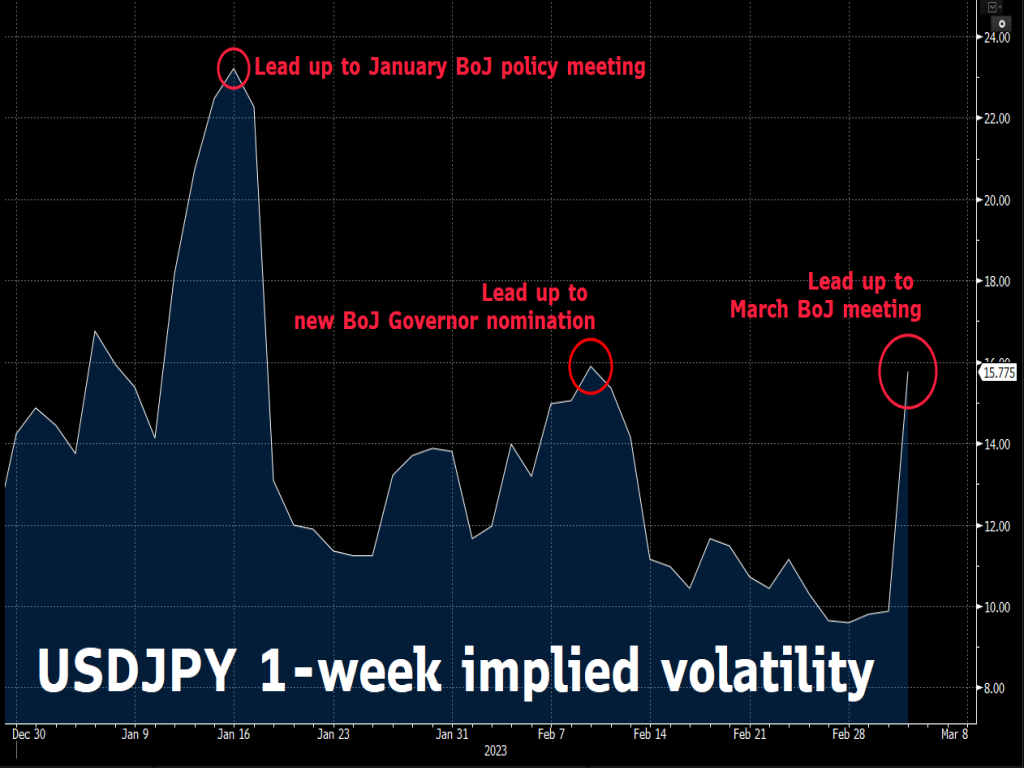

The Japanese Yen is expected to be the most volatile among its G10 peers versus the US dollar over the next one week.

The one-week implied volatility for USDJPY is duly rising again in the lead up to the March 10th Bank of Japan policy meeting – the last one for outgoing BoJ Governor Haruhiko Kuroda.

To be clear, markets aren’t expecting any policy changes (no rate hikes, no tweaks to yield curve control) for next week’s BoJ meeting.

Yet, traders are already on edge on rumours that Kuroda may deliver another surprise policy change as his final salvo before leaving the hot seat.

And why might Kuroda do just that?

Governor Kuroda may have to do the “dirty job” of rocking markets next week.

This would give markets time to digest an out-of-the-blue move, before handing over the reins of Japanese monetary policy in a calmer fashion to his successor, Kazuo Ueda, on April 9th.

Also, keep in mind that the BoJ has shown a penchant for shocking markets over the decades, including:

-

surprise rate hike on Christmas Day 1989

-

Kuroda’s bond purchase boost in 2014

- Kuroda’s tweak to the yield curve control in December 2022

One final policy surprise before he steps down wouldn’t be uncharacteristic for Kuroda, and that could translate into big moves for the Japanese Yen.

Bloomberg FX model: 72% chance that USDJPY trades within 133.41 – 139.64 range next week.

2) AUDUSD

The Reserve Bank of Australia is expected to hike its cash rate by another 25 basis points, bringing it up to 3.6%.

However, the surprise slowdown in Australia’s January inflation data as well as last quarter’s (Q4 2022) GDP print suggest that the economy is already feeling the strain from the RBA’s rate hikes totaling 325 basis points since May 2022.

-

If the RBA actually stands pat on the cash rate, amid rising concerns of incurring too much economic damage, that may heap more downward pressure on AUDUSD.

- On the other hand, if the RBA signals its intent to keep pressing ahead with even more rate hikes to cool down problematic inflation, that could see an uplift in AUDUSD.

Bloomberg FX model: 72% chance that AUDUSD trades within 0.6628 – 0.6867 range next week.

3) USDCAD

Referring back to the Bloomberg chart above of 1-week implied volatilities for G10 currencies vs. the US dollar …

The Canadian Dollar is set to have the mildest week relative to its G10 peers.

After all, Bank of Canada governor Tiff Macklem had already signaled a pause in rate hikes at the central bank’s previous meeting in January.

For next week’s meeting, the Bank of Canada is expected to stand pat on its benchmark rate, keeping it at 4.5% - its highest level in 15 years.

Then comes Canada’s jobs report on Friday.

Weaker-than-expected Canadian employment data, which then threatens to widen the policy gap between a BoC that’s on pause versus a still-aggressive Federal Reserve … could see the Canadian Dollar lose out on its title as the smallest-loser against the US dollar so far this year.

Bloomberg FX model: 72% chance that AUDUSD trades within 0.6628 – 0.6867 range next week.