This week’s highly-awaited major central bank decisions have come and gone.

And all 3 major central banks largely adhered to market expectations for the respective rate hikes.

After all, policymakers were certainly aware that market nerves are still raw after enduring the financial turmoil on both sides of the Atlantic, engulfing names like Silicon Valley Bank and Credit Suisse.

It wouldn’t have been in their best interests to spook markets further.

Hence, the following rate decisions resulted in relatively subdued volatility in FX markets.

Before we recap the various central bank decisions, first a reminder:

- FX markets tend to "reward" and strengthen the currency of the central bank that can push its own interest rates higher (relative to other economies)

- However, as we've seen of late, a currency's movements also can be driven by market sentiment surrounding its economic performance. When confidence is weak, that tends to translate into currency weakness.

Hence, no surprise that the US dollar and the Swiss Franc were roiled amid the sudden chaos engulfing Silicon Valley Bank and Credit Suisse over the past two weeks.

Now time for the recap, starting with the most recent:

The Bank of England (BOE) hiked by 25 basis points (bps).

Just an hour ago, the BOE was also able to sound a hawkish note and signal more UK rate hikes ahead, while forecasting that the UK economy will dodge a recession this year.

After all, the UK January consumer price index (used to measure headline inflation) that was released yesterday (Wednesday, March 22nd) showed that inflation remains stubbornly in double-digit territory. The CPI climbed by 10.4% in January 2023, compared to January 2022 (year-on-year).

Such an outlook by the central bank helped GBPUSD sustain recent gains.

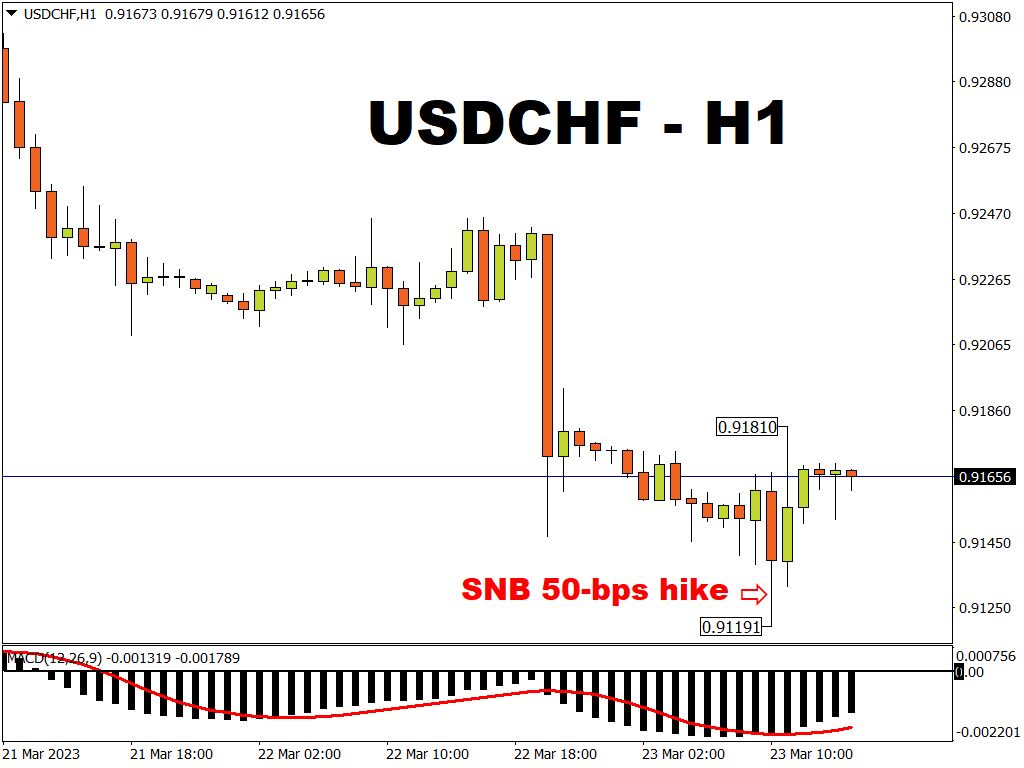

The Swiss National Bank (SNB) hiked by 50 bps.

Also today (Thursday, March 23rd), the SNB prioritised its fight against inflation and suggested that more rate hikes are incoming.

The SNB issued such hawkish signals despite the recent financial turmoil surrounding Credit Suisse.

Still, today’s rate hike was unable to prevent the Swiss Franc from weakening against its G10 peers.

Despite the CHF strength as the immediate reaction to the lager 50bps hike by the SNB (relative to the Fed and BOE), the Swiss Franc was unable to hold on to those gains against the US dollar.

The US Federal Reserve (Fed) hiked by 25 bps.

On Wednesday, Fed Chair Jerome Powell insisted that policymakers remain focused on conquering inflation with more rate hikes.

However, markets were willing to challenge Powell’s narrative!

Markets now pricing in a 70% chance that the Fed would actually CUT interest rates in July 2023!

Such dovish repricing pushed the US dollar index down to its lowest levels since early February, and the greenback is still evidently struggling today.

What’s next for FX markets?

Investors and traders will still be busy deciphering the next moves by these major central bankers.

And such outlooks will be informed via the regular menu of tier-1 economic data out (think inflation and jobs data)of these major economies.

Of course, markets will also be keeping a close eye on signs of further instability in the US and European banking sectors.

If the contagion spreads and sends the global financial system into yet another crisis, that would roil global financial markets.

Ultimately, as mentioned earlier, markets are likely to weaken the currency that’s closest to ground zero of the financial turmoil, as the US Dollar and the Swiss Franc experienced in recent weeks.

On the flip side, should investors and traders make a run for the hills, safe havens such as gold and the Japanese Yen should ultimately benefit.